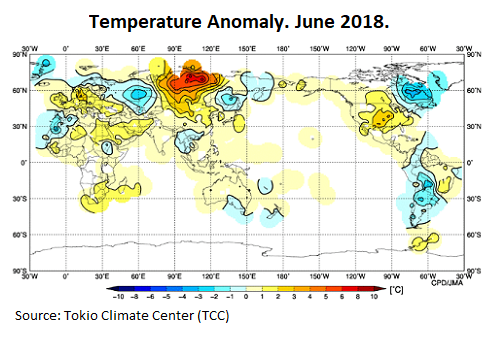

The world is going through a heat wave that affects the main wheat producing countries worldwide. An adverse weather is hitting the Valley of Death as well as cities located in Algeria, Japan, Germany, Hong Kong, Norway, Sweden, among others.

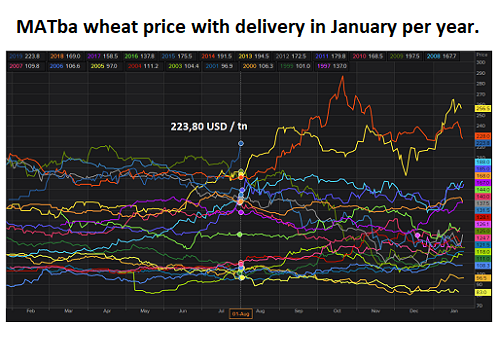

Productive problems in the main producing countries such as the European Union, Ukraine and Russia, become more evident as the cereal crop harvest takes place and weather complications deteriorate the status of the crops while the reported bears are lower than those expected. The adverse climate conditions generated a strong upward pressure on the price for wheat placed in the main ports worldwide, including the FOB price in Argentine ports. Locally, the FOB price of wheat at harvest relieved by the Ministry of Agribusiness increased U$S 27/t in only 15 days, reaching U$S 226/t on August 1st. The bullish movement in the price of wheat in the international markets dragged in tune the 2018/19 wheat price in the local market. 2018/19 wheat prices at MATba (using contracts with delivery in January in Buenos Aires, for a historical analysis purpose), are already the highest, to August 1st of each year, since there is record in 1997.

Productive problems in the main producing countries such as the European Union, Ukraine and Russia, become more evident as the cereal crop harvest takes place and weather complications deteriorate the status of the crops while the reported bears are lower than those expected. The adverse climate conditions generated a strong upward pressure on the price for wheat placed in the main ports worldwide, including the FOB price in Argentine ports. Locally, the FOB price of wheat at harvest relieved by the Ministry of Agribusiness increased U$S 27/t in only 15 days, reaching U$S 226/t on August 1st. The bullish movement in the price of wheat in the international markets dragged in tune the 2018/19 wheat price in the local market. 2018/19 wheat prices at MATba (using contracts with delivery in January in Buenos Aires, for a historical analysis purpose), are already the highest, to August 1st of each year, since there is record in 1997.

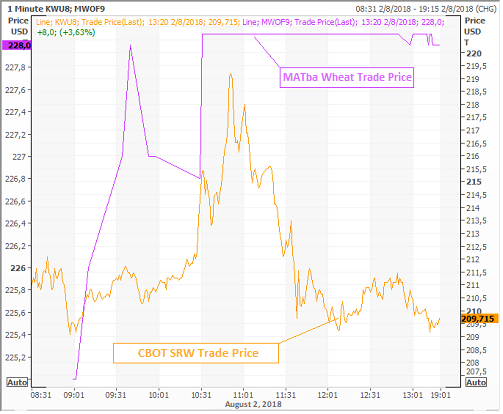

On Thursday, August 2, the price of MATba wheat increased even more, U$S 8/t in almost all the deferred positions (both in Rosario and Buenos Aires), reaching the maximum allowed daily price movement, which made the operation close immediately. This strong increase in the price responded to the prices traded in CBOT and other markets around the world. At midday, Chicago SRW wheat contracts added up to more than U$S 10/t due to the rumors that Ukraine could limit wheat exports after the adverse weather that affected wheat in its critical period of development and during the harvest.

On Thursday, August 2, the price of MATba wheat increased even more, U$S 8/t in almost all the deferred positions (both in Rosario and Buenos Aires), reaching the maximum allowed daily price movement, which made the operation close immediately. This strong increase in the price responded to the prices traded in CBOT and other markets around the world. At midday, Chicago SRW wheat contracts added up to more than U$S 10/t due to the rumors that Ukraine could limit wheat exports after the adverse weather that affected wheat in its critical period of development and during the harvest.

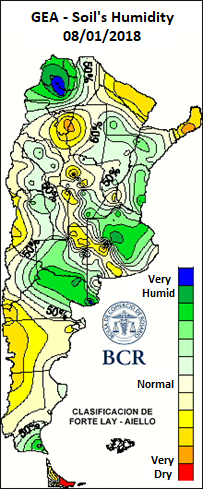

Shortly after the price rebound, the Minister of Agriculture of Ukraine strongly denied these rumors, which cut the profits in the North American market, but not in the local market. Meanwhile, according to what is said by analysts of the Russian market, similar rumors would have transcended about Russia's foreign trade in a very similar scenario. Wheat crop progress in Argentina. Reaching the end of the sowing season, it can be projected a high productivity scenario for Argentine wheat. In principle, soil reserves are optimal for the phenological phase that is taking place: from foliation to full tillering. Low temperatures encourage the formation of tillers while limiting the progress of diseases. There is aphid presence but not at disturbing levels. Producers focus on the fact that the crop has an adequate dose of nitrogen in order to reach a good level of yield and quality. The sowing comes to cover, almost without any difficulties, almost 98% of the intentional productive area.

Shortly after the price rebound, the Minister of Agriculture of Ukraine strongly denied these rumors, which cut the profits in the North American market, but not in the local market. Meanwhile, according to what is said by analysts of the Russian market, similar rumors would have transcended about Russia's foreign trade in a very similar scenario. Wheat crop progress in Argentina. Reaching the end of the sowing season, it can be projected a high productivity scenario for Argentine wheat. In principle, soil reserves are optimal for the phenological phase that is taking place: from foliation to full tillering. Low temperatures encourage the formation of tillers while limiting the progress of diseases. There is aphid presence but not at disturbing levels. Producers focus on the fact that the crop has an adequate dose of nitrogen in order to reach a good level of yield and quality. The sowing comes to cover, almost without any difficulties, almost 98% of the intentional productive area.

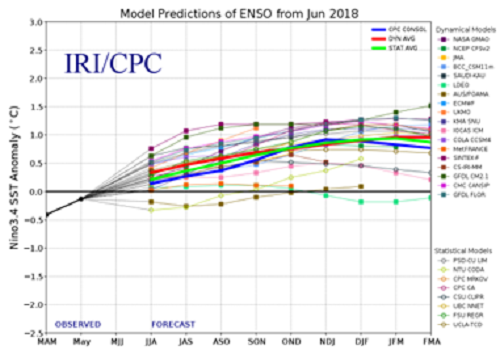

Medium-term forecasts indicate the presence of a normal ENSO for this winter and a slight Niño for the warmer months. However, it must be borne in mind that the atmospheric system is very unstable due to global warming, therefore weeks without rain should not be ruled out for the spring.

Medium-term forecasts indicate the presence of a normal ENSO for this winter and a slight Niño for the warmer months. However, it must be borne in mind that the atmospheric system is very unstable due to global warming, therefore weeks without rain should not be ruled out for the spring.

Rosario's Cash Market At Rosario's cash market, due to the mentioned factors, wheat had a bullish week both in the spot market as well as in the forward market. Rosario Board of Trade's reference price showed a weekly increase, reaching U$S 217/t on Thursday, August 2. Meanwhile, buyers' open offers for wheat with delivery in December passed from a value of between 205 and 210 dollars on Thursday, July 26, to reaching U$S 225/t a week later, in other words, a weekly profit of approximately fifteen dollars. This context encouraged a fluid business development at Rosario Board of Trade's cash market, for new wheat mainly, but the business for the cereal with available delivery was not insignificant either.

Rosario's Cash Market At Rosario's cash market, due to the mentioned factors, wheat had a bullish week both in the spot market as well as in the forward market. Rosario Board of Trade's reference price showed a weekly increase, reaching U$S 217/t on Thursday, August 2. Meanwhile, buyers' open offers for wheat with delivery in December passed from a value of between 205 and 210 dollars on Thursday, July 26, to reaching U$S 225/t a week later, in other words, a weekly profit of approximately fifteen dollars. This context encouraged a fluid business development at Rosario Board of Trade's cash market, for new wheat mainly, but the business for the cereal with available delivery was not insignificant either.