South America as the leading exporting crusher in soybean complex

PATRICIA BERGERO-BLAS ROZADILLA

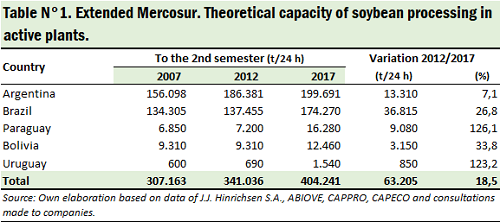

In South America, among 10 countries can process 134 Mt of soybeans, but Argentina and Brazil have 92% of that capacity Argentina, Bolivia, Brazil, Paraguay and Uruguay have jointly a theoretical capacity to process oilseeds of 404,241 tons per day; all in plants that were active at some time in the previous year. This means that the region can process 133.4 Mt of oilseeds per year, a capacity that would be used in 69% as it is estimated at 92.6 Mt of grinding in 2017/2018. Argentina and Brazil have installed plants that cover 92% of the industrialization capacity of all South America, and of those two countries Argentina itself has 50%. The five countries mentioned are not the only ones that process soybeans, since Chile, Colombia, Ecuador, Peru and Venezuela process between 850 and 900 thousand tons jointly - 60% is carried out by Colombia - so they have the facilities to carry out that industrial process. The analysis from now on is concentrated in the group called Extended Mercosur (Mercosur Ampliado, in Spanish), considering that the region already includes the 4G (Argentina, Bolivia, Brazil and Paraguay, as the main producers and exporters processors of the soybean complex) and Uruguay, despite that Bolivia is in the process of joining the original integration bloc (Argentina, Brazil, Paraguay and Uruguay). In 10 years, the capacity grew 32%; the largest increase was 18.5% in the five-year period 2012 - 2017 A decade ago, the South American oleaginous complex industry had an active processing capacity of 307,163 t per day. From this data, it can be seen that the productive capacity has grown by more than 97,000 tons in the last 10 years; or, said in other terms, by 32%. However, when analyzing the evolution in five-year periods, it can be seen that the most significant jump occurred between 2012 and 2017, when more than 63 thousand tons were added to the installed capacity (18.5%).

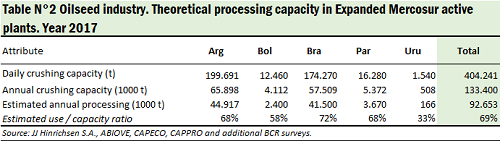

These figures include only the capacity of the plants that are active, or, at least, that worked at some time during the year preceding the cut of the information. For the data, several sources were used, among which the most important is the yearbook of the FOB broker J.J. Hinrischsen S.A. In addition, information provided by ABIOVE has been used in Brazil; CAPECO and CAPPRO, in Paraguay; and of what arises from consultations with experts, analysts and officials of companies in the sector to complete the information. Always taking the last five years, due to the strong increase in capacity, it can be seen that the largest expansion for processing was in Brazil, if absolute values are considered. In that country, capacity was increased by 36,815 tons per day, which represents 59% of the increase experienced by the region. If the relative terms are considered, Paraguay and Uruguay were the ones that had the greatest growth in their capacity. Both countries more than doubled their soy processing potential; Uruguay had an increase of 123.2%, while in Paraguay the capacity of the oilseed processing industry grew by 126.1%. In the case of Argentina, although it registered the smallest five-year percentage increase at the end of 2017 (7.1%) and lost some relative weight (it went from 55% to 50%), its active processing capacity is still half that of the one existing in all South America. In fact, the location of the oil plants in the port terminals of the Gran Rosario means that the concentrated capacity exceeds all the tonnage installed in Brazil, which is the second South American crusher. Brazil with the best use / capacity ratio in 2017 with 72%; Argentina and Paraguay with 68% Table 2 shows the calculation of the degree of utilization of the theoretical capacity installed in each of the countries in 2017, based on the quantity of tons actually processed. There can be seen that Brazil is the nation that has made the greatest use of its installed capacity, since this ratio is 72%. Then there comes Paraguay and Argentina, both with 68% of capacity used. Bolivia follows with 58% and Uruguay closes with 33%. Taken as a whole, this Expanded Mercosur would have used 69% of its total capacity in 2017. It should be mentioned that for Argentina, to the extent that local plants can process other oilseeds and there is a high production of sunflower, the processing of other oilseeds reduces the idle capacity and therefore they are taken into account in the attached table. Considering the industrialization of 2017, the installed capacity / use ratio amounted to 68%, but if only soy were used, that ratio would be 63%. Another point not less to consider when looking at these figures is that those plants of smaller scale do not work in a sustained manner over a year.

These figures include only the capacity of the plants that are active, or, at least, that worked at some time during the year preceding the cut of the information. For the data, several sources were used, among which the most important is the yearbook of the FOB broker J.J. Hinrischsen S.A. In addition, information provided by ABIOVE has been used in Brazil; CAPECO and CAPPRO, in Paraguay; and of what arises from consultations with experts, analysts and officials of companies in the sector to complete the information. Always taking the last five years, due to the strong increase in capacity, it can be seen that the largest expansion for processing was in Brazil, if absolute values are considered. In that country, capacity was increased by 36,815 tons per day, which represents 59% of the increase experienced by the region. If the relative terms are considered, Paraguay and Uruguay were the ones that had the greatest growth in their capacity. Both countries more than doubled their soy processing potential; Uruguay had an increase of 123.2%, while in Paraguay the capacity of the oilseed processing industry grew by 126.1%. In the case of Argentina, although it registered the smallest five-year percentage increase at the end of 2017 (7.1%) and lost some relative weight (it went from 55% to 50%), its active processing capacity is still half that of the one existing in all South America. In fact, the location of the oil plants in the port terminals of the Gran Rosario means that the concentrated capacity exceeds all the tonnage installed in Brazil, which is the second South American crusher. Brazil with the best use / capacity ratio in 2017 with 72%; Argentina and Paraguay with 68% Table 2 shows the calculation of the degree of utilization of the theoretical capacity installed in each of the countries in 2017, based on the quantity of tons actually processed. There can be seen that Brazil is the nation that has made the greatest use of its installed capacity, since this ratio is 72%. Then there comes Paraguay and Argentina, both with 68% of capacity used. Bolivia follows with 58% and Uruguay closes with 33%. Taken as a whole, this Expanded Mercosur would have used 69% of its total capacity in 2017. It should be mentioned that for Argentina, to the extent that local plants can process other oilseeds and there is a high production of sunflower, the processing of other oilseeds reduces the idle capacity and therefore they are taken into account in the attached table. Considering the industrialization of 2017, the installed capacity / use ratio amounted to 68%, but if only soy were used, that ratio would be 63%. Another point not less to consider when looking at these figures is that those plants of smaller scale do not work in a sustained manner over a year.

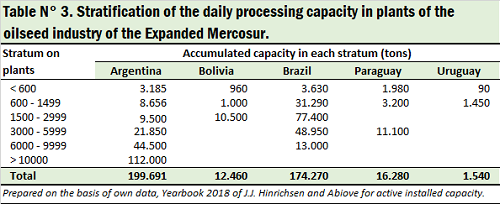

Looking from a comparative point of view, the information in table 2 shows a lower utilization of capacity compared to the previous year, since in 2016 the capacity used in the Expanded Mercosur had been 73%. According to the estimates made, only Paraguay would have improved its efficiency in the use of its productive infrastructure, since it went from 60% to 68% in that ratio. Argentina, which showed a level of utilization of 69% in 2016, would have reported a level of 68% for 2017. The "great" scale: 56% of the installed capacity in Argentina is in plants that can process more than 10,000 t daily As can be seen in Table 3, 56% of the active installed capacity in Argentina is concentrated in facilities above 10,000 t. If you add plants that are between 3,000 and 9,999 t, 89% corresponds to facilities of medium to large size. This is directly related to an industry that was cemented with an export destination, as opposed to what happens in Brazil, where the plants that are in the 3,000 to 9,999 t stratum represent 36% of the total.

Looking from a comparative point of view, the information in table 2 shows a lower utilization of capacity compared to the previous year, since in 2016 the capacity used in the Expanded Mercosur had been 73%. According to the estimates made, only Paraguay would have improved its efficiency in the use of its productive infrastructure, since it went from 60% to 68% in that ratio. Argentina, which showed a level of utilization of 69% in 2016, would have reported a level of 68% for 2017. The "great" scale: 56% of the installed capacity in Argentina is in plants that can process more than 10,000 t daily As can be seen in Table 3, 56% of the active installed capacity in Argentina is concentrated in facilities above 10,000 t. If you add plants that are between 3,000 and 9,999 t, 89% corresponds to facilities of medium to large size. This is directly related to an industry that was cemented with an export destination, as opposed to what happens in Brazil, where the plants that are in the 3,000 to 9,999 t stratum represent 36% of the total.

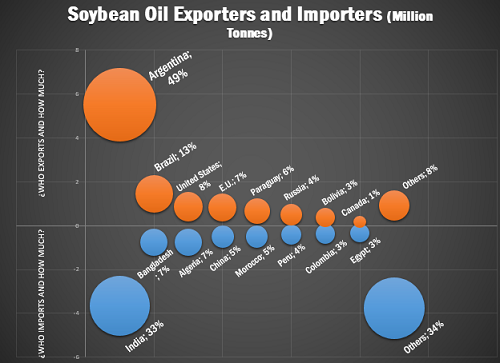

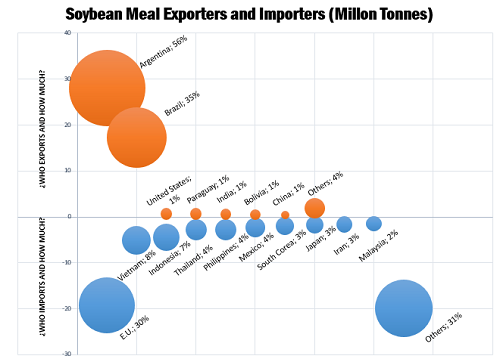

The plant of 3,000 t is taken as a point from which significant changes are observed of what is happening in South America, and particularly in exporting producing countries such as Argentina, based on references from specialists. It is worth mentioning what was presented by an industry specialist such as Tim Kemper, director of global operations for Desmet Ballestra, in a presentation at an international conference five years ago. While there may be many changes in the five years since the Belgian company is leader in engineering services and acquisition of oilseed processing plants in the world, there are figures that give an idea of what kind of capabilities are installed for soy in the world . At that time, Kemper mentioned that from the new plants sold in 5 years (32 for soybeans), there was certainly a growth in scale, which for that period the average installed capacity was 2,850 t and the median was 1,900 t. 7.5 out of 10 ships carry South American soybean meal and oil; 5 are products of Argentine origin Returning to the issue of increases in installed capacity, the targeting of these increases in the period from 2012 to 2017 says a lot about the opportunity used by the soy-producing countries neighboring Argentina, in terms of reception who had the investments. However, it also says a lot about the opportunity lost in our country to stimulate the local crushing industry to capture the productive surpluses of soy from those same countries to turn them into products. The current context in Argentina is different and beyond the unfavorable situation in terms of supply of oilseeds by virtue of the drought, the region, or more specifically Argentina, will continue to lead the international trade in oil and soybean meal (see attached graphs). This leadership is based on the model of a large scale, modern and efficient industry installed near the terminal points of shipment, to process in the country of origin and place the products in the international arena.

The plant of 3,000 t is taken as a point from which significant changes are observed of what is happening in South America, and particularly in exporting producing countries such as Argentina, based on references from specialists. It is worth mentioning what was presented by an industry specialist such as Tim Kemper, director of global operations for Desmet Ballestra, in a presentation at an international conference five years ago. While there may be many changes in the five years since the Belgian company is leader in engineering services and acquisition of oilseed processing plants in the world, there are figures that give an idea of what kind of capabilities are installed for soy in the world . At that time, Kemper mentioned that from the new plants sold in 5 years (32 for soybeans), there was certainly a growth in scale, which for that period the average installed capacity was 2,850 t and the median was 1,900 t. 7.5 out of 10 ships carry South American soybean meal and oil; 5 are products of Argentine origin Returning to the issue of increases in installed capacity, the targeting of these increases in the period from 2012 to 2017 says a lot about the opportunity used by the soy-producing countries neighboring Argentina, in terms of reception who had the investments. However, it also says a lot about the opportunity lost in our country to stimulate the local crushing industry to capture the productive surpluses of soy from those same countries to turn them into products. The current context in Argentina is different and beyond the unfavorable situation in terms of supply of oilseeds by virtue of the drought, the region, or more specifically Argentina, will continue to lead the international trade in oil and soybean meal (see attached graphs). This leadership is based on the model of a large scale, modern and efficient industry installed near the terminal points of shipment, to process in the country of origin and place the products in the international arena.