Some considerations on Argentina’s new export taxes scheme

PATRICIA BERGERO – EMILCE TERRÉ

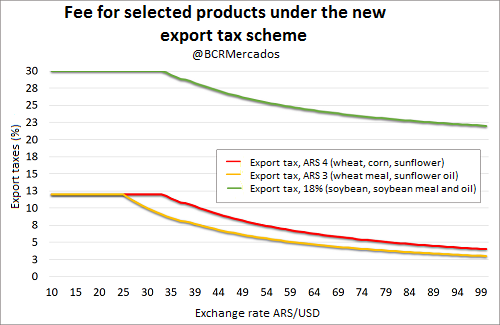

According to the Decree 793/2018, every exported product will pay a tax of 12% on its taxable value or, in the case of most agribusiness products, on the FOB price. However, the fee has a maximum of 4 ARS for every dollar exported (taxable value or FOB price), although for some goods in particular, it applies a lower maximum of 3 ARS per dollar exported. The 4 ARS fee applies to all primary products or low-processed goods, including live animals, grains and oilseeds, legumes, yerba mate, tea, flowers, vegetables , fruits, etc., and some industrial products, such as honey, soybean oil and meal and soy pellets. Meanwhile, the lower 3 ARS fee applies to a large part of industrial products and services, including meat, fish, dairy products, eggs, etc. As for the soybean complex, the main generator of dollars through international trade in Argentina, the new taxation scheme complements the previous one. Products such as soybeans, oil or meal will pay 18% (existing export tax) plus 12% or the cap of 4 ARS per dollar exported. Biodiesel, on the other hand, will pay 15% plus 12% or the cap of 4 ARS per dollar exported. Finally, certain products used for animal feed containing soybeans will pay 11-16% plus 12% or the cap of 3 ARS per dollar exported. While establishing a nominal fixed fee for every dollar exported (that is, for an export good that worth US$ 100, taxes will reach ARS 400), the taxable value will always be proportional to the product value, but not to the value of US dollar (exchange rate). Therefore, the weight of the tax rate would decrease as the price of US dollar rises. The following table shows the tax rate evolution for soybean, sunflower and corn complex in different exchange rate scenarios. In the case of the soybean complex, given an exchange rate of 33.3 ARS/USD or lower, the fee becomes maximum at a fixed percentage of 30%. From this exchange rate upwards, the weight of the export tax decreases. For instance, at 40 ARS/USD the fee would be around 28%, while at 50 ARS/USD it would drop to 26%, and so on. From this point of view, there is no incentive to add value to products since soymeal and oil pay the same fees as soybeans. In the case of other grains, at a 33.3 ARS/USD or lower, export tax reaches the maximum and is set at 12%, while if US dollar value is above this mark the weight of taxation tends to fall. In the case of wheat complex, similarly, export taxes fall as the exchange rate rises.

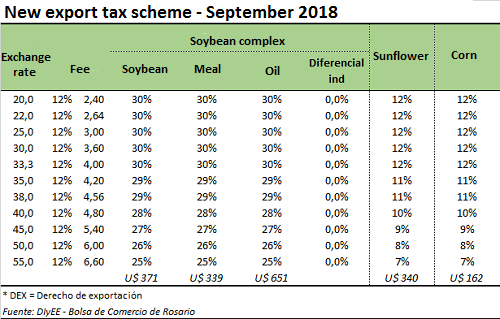

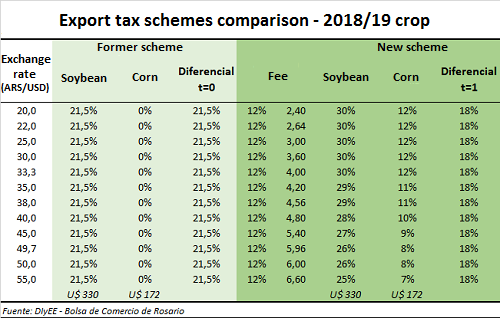

The following table shows the effective rate evolution for different agribusiness products and by-products. As the exchange rate falls (the ARS gains value), the tax increases, and on the contrary, as the exchange rate rises (the ARS loses value), the tax burden decreases.

The following table shows the effective rate evolution for different agribusiness products and by-products. As the exchange rate falls (the ARS gains value), the tax increases, and on the contrary, as the exchange rate rises (the ARS loses value), the tax burden decreases.