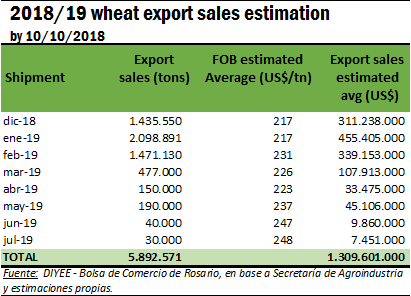

Up to October 10, wheat exporters have sold 5.9 million tons abroad, to be shipped between December 2018 and July 2019. Measured in US dollars, this is close to US$ 1,305 million. 85% of these commitments (US $ 1,106 million) would be shipped in the quarter from December 2018 to February 2019, matching the main harvest period.

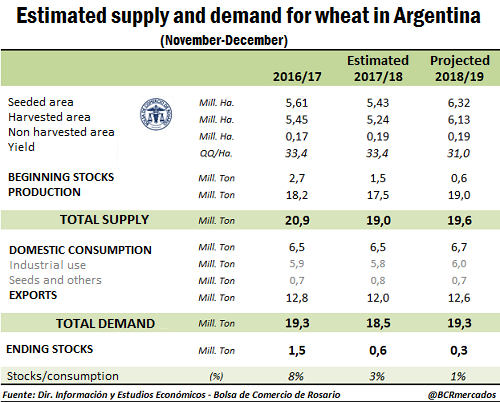

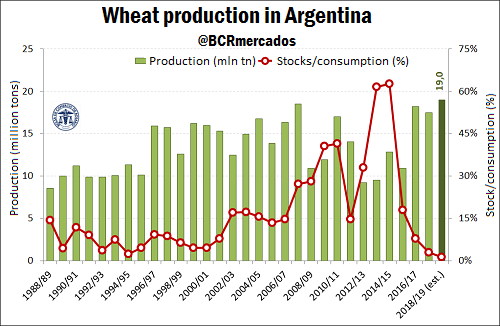

Based on an estimated production of 19 million tons in the 2018/19 crop year, and foreseeing excellent prospects for international demand in the face of the stocks shortcut in some of the world's main cereal suppliers, Argentina's total exports could be around 12.6 million tons; 5% above 2017/2018 but still below the historical record of 12.8 Mt reached in the 2016/17 commercial year.

Based on an estimated production of 19 million tons in the 2018/19 crop year, and foreseeing excellent prospects for international demand in the face of the stocks shortcut in some of the world's main cereal suppliers, Argentina's total exports could be around 12.6 million tons; 5% above 2017/2018 but still below the historical record of 12.8 Mt reached in the 2016/17 commercial year.

This is because beginning stocks will be tight on next commercial year, just 600,000 tons. Thus, although production would still be an all-time record, the total supply of 19.6 Mt would be lower than the maximum of 20.9 Mt reached in 2016/17.

This is because beginning stocks will be tight on next commercial year, just 600,000 tons. Thus, although production would still be an all-time record, the total supply of 19.6 Mt would be lower than the maximum of 20.9 Mt reached in 2016/17.

If these estimates are met, 2018/19 final stocks would reach a historical minimum, leaving the stock / consumption ratio in just 1%. Low stocks combined with a strong demand are usually associated with periods of high volatility in prices, making hedges advisable to minimize its impact on companies´ results.

If these estimates are met, 2018/19 final stocks would reach a historical minimum, leaving the stock / consumption ratio in just 1%. Low stocks combined with a strong demand are usually associated with periods of high volatility in prices, making hedges advisable to minimize its impact on companies´ results.