In Chicago, soybeans reached 2008 lows Throughout the month of June, soybean negotiated in Chicago suffered a sharp drop, as a result of the commercial conflict that develops between the main world powers, the United States and China. The good state of the crops in the North American country also pressured prices. Last Thursday, the prices reached minimums from the end of 2008.

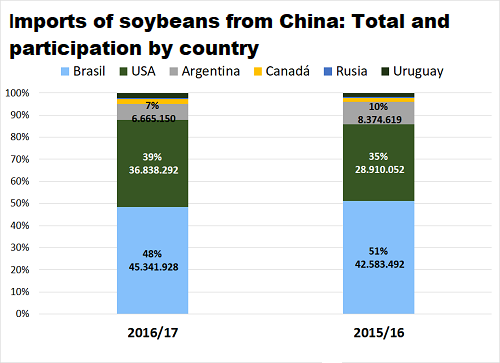

The question we can ask ourselves from South America is, why, this trade conflict between China and the United States (affecting the price of US soy), has to affect the price of soy in the ports of Argentina, and to a lesser extent in Brazil, among other origins. The first problem that this conflict causes in the markets is greater uncertainty, because we do not know for sure what could happen in the medium term. The conflict is likely to escalate to larger instances, increasing the quantities of products that would be under tariffs or para-tariff barriers, deepening the negative impact on the growth of both countries and dragging along global growth. Market sources point out that the Asian giant has been actively seeking for soybeans from other alternative destinations, such as Russia, Ukraine and even India. The same goes for Brazil's bean demand, indicating that a larger portion of the soybean exports from the neighboring country will go to China. The latter means that even Brazil has to import soy from the United States. According to market sources in Brazil, this year they would have to import between 0.5 and 1 Millon tons of soy from the US to supply the demand of local processors. According to a Rabobank report, in the remainder of the 17/18 commercial year, China has the possibility to close all of its projected purchases by acquiring a large part of the stocks from Brazil. The total of the projected imports for China would be reached despite the severe drought that Argentina suffered. USA is an indispensable supplier, since it provides between 35% and 40% of China's total imports, only passed by Brazil. The problem looms over the next 18/19 crop year (Oct-Sep). Due to excessive tariffs on US soybeans, China will have to import from alternative destinations, process another type of oilseed or import soybean meal.

The question we can ask ourselves from South America is, why, this trade conflict between China and the United States (affecting the price of US soy), has to affect the price of soy in the ports of Argentina, and to a lesser extent in Brazil, among other origins. The first problem that this conflict causes in the markets is greater uncertainty, because we do not know for sure what could happen in the medium term. The conflict is likely to escalate to larger instances, increasing the quantities of products that would be under tariffs or para-tariff barriers, deepening the negative impact on the growth of both countries and dragging along global growth. Market sources point out that the Asian giant has been actively seeking for soybeans from other alternative destinations, such as Russia, Ukraine and even India. The same goes for Brazil's bean demand, indicating that a larger portion of the soybean exports from the neighboring country will go to China. The latter means that even Brazil has to import soy from the United States. According to market sources in Brazil, this year they would have to import between 0.5 and 1 Millon tons of soy from the US to supply the demand of local processors. According to a Rabobank report, in the remainder of the 17/18 commercial year, China has the possibility to close all of its projected purchases by acquiring a large part of the stocks from Brazil. The total of the projected imports for China would be reached despite the severe drought that Argentina suffered. USA is an indispensable supplier, since it provides between 35% and 40% of China's total imports, only passed by Brazil. The problem looms over the next 18/19 crop year (Oct-Sep). Due to excessive tariffs on US soybeans, China will have to import from alternative destinations, process another type of oilseed or import soybean meal.

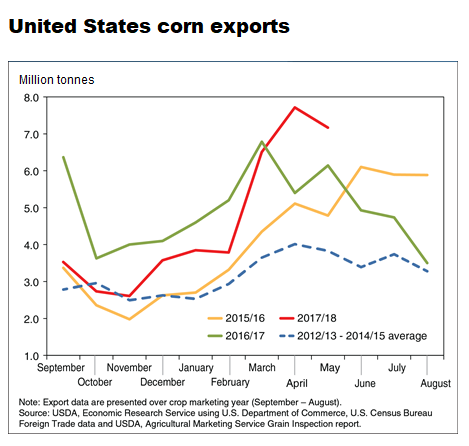

The lower availability of oilseeds in other countries will not be enough to cover the gap caused by import tariffs. Rabobank analysts expect that China's total import volume of soybean will experience a year-on-year decline, with a bigger Brazil's share in total imports. In addition, China's processing plants will have no choice but to buy between 10 and 15 million tons of US soy, subject to tariffs. According to this report, in the long term, if tariffs remain high, the global supply of soybeans should be able to adjust accordingly. The area planted with soybeans in the USA would considerably decrease, while the area sown in South America would increase. In the Northern Hemisphere, the Black Sea region also has potential to expand soybean acreage. As for China, the commercialization of genetically modified soy could be an option to boost national production and decrease the dependence on imports. If tariffs are maintained for years to come, China's soybean imports could be reduced, due to: 1. Bigger national production of soy 2. More imports of protein meals and other oilseeds 3. Improve the feed conversion ratio, which leads to less use of food The drought in Argentina and then in Brazil boosts shipments of US corn. United States corn exports reached a record high in April of 7.7 million tons (Mt). Maize shipments from September to May are estimated at 29 Mt while USDA projections for US exports in the 17/18 crop year (September-August) rose to 58.4 Mt in its latest report. The previous monthly record of exports dates from November 1989, almost 30 years ago. Projections for May exports, based on inspections, are higher than usual at this time of year, suggesting continued strength in the United States corn export market. This is due, in part, to the continuing drought in Argentina, an important supplier of corn, which reduced the export prospects from last year. In addition, second-season corn in Brazil is expected to have problems, reflecting dry weather and a smaller sown area. As a result, importing countries have fewer options, which increases US competitiveness. The main US destinations, as accumulated in 2017/18 are: Mexico (27% of the total), Japan (20%), Colombia (11%), South Korea (8%), Peru (6 %), among others.

The lower availability of oilseeds in other countries will not be enough to cover the gap caused by import tariffs. Rabobank analysts expect that China's total import volume of soybean will experience a year-on-year decline, with a bigger Brazil's share in total imports. In addition, China's processing plants will have no choice but to buy between 10 and 15 million tons of US soy, subject to tariffs. According to this report, in the long term, if tariffs remain high, the global supply of soybeans should be able to adjust accordingly. The area planted with soybeans in the USA would considerably decrease, while the area sown in South America would increase. In the Northern Hemisphere, the Black Sea region also has potential to expand soybean acreage. As for China, the commercialization of genetically modified soy could be an option to boost national production and decrease the dependence on imports. If tariffs are maintained for years to come, China's soybean imports could be reduced, due to: 1. Bigger national production of soy 2. More imports of protein meals and other oilseeds 3. Improve the feed conversion ratio, which leads to less use of food The drought in Argentina and then in Brazil boosts shipments of US corn. United States corn exports reached a record high in April of 7.7 million tons (Mt). Maize shipments from September to May are estimated at 29 Mt while USDA projections for US exports in the 17/18 crop year (September-August) rose to 58.4 Mt in its latest report. The previous monthly record of exports dates from November 1989, almost 30 years ago. Projections for May exports, based on inspections, are higher than usual at this time of year, suggesting continued strength in the United States corn export market. This is due, in part, to the continuing drought in Argentina, an important supplier of corn, which reduced the export prospects from last year. In addition, second-season corn in Brazil is expected to have problems, reflecting dry weather and a smaller sown area. As a result, importing countries have fewer options, which increases US competitiveness. The main US destinations, as accumulated in 2017/18 are: Mexico (27% of the total), Japan (20%), Colombia (11%), South Korea (8%), Peru (6 %), among others.

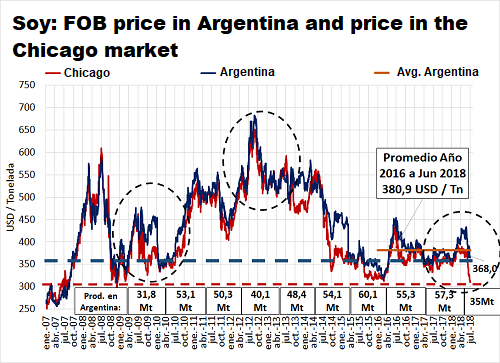

Corn and soybean activity in the local market In the week, the Rosario Board of Trade´s soybeans reference price was of USD 279 / t on Thursday, July 5, noting a recovery of 2.64 USD / t compared to the previous week. The price of soybeans at the local level remains constant with the export prices of soy by-products that remain stable. This price stability occurs despite the fall in the price of soybean traded in the Chicago market (-9.5 USD / tn), oil byproducts (-12 USD / tn) and flour (-4, USD 75 / tn). As discussed above, although a world reference price for soy is negotiated in Chicago, it does not indicate that prices in local markets move in the same way. In recent weeks there has been a strong pace of purchases from the industries, and by-prudoducts´ FOB export prices remained constant, supporting the payment capacity of the "oil industry". This is due to an increase in by-products´ export premiums that offset the drops in Chicago. Thus, since the beginning of June, soybeans in Chicago have been dropping approx. 67 USD / tn, while the industry's ability to pay fell approx. 38 USD / tn. Regarding the commercialization, the export and industrial sectors have purchased 24.6 Mt of the 2017/18 soybeans, equivalent to 70% of the total production. The pace of purchases remains far above previous years. It can be seen on the other hand that, despite the "closing of the North American market" for imports from China, Argentine soybean external sales have not accelerated in recent weeks. At the end of June, soybean export sales barely reached 1.29 Mt. The damage suffered by the local soybean harvest is evident, not only because of its volume, but also in terms of its quality.

Corn and soybean activity in the local market In the week, the Rosario Board of Trade´s soybeans reference price was of USD 279 / t on Thursday, July 5, noting a recovery of 2.64 USD / t compared to the previous week. The price of soybeans at the local level remains constant with the export prices of soy by-products that remain stable. This price stability occurs despite the fall in the price of soybean traded in the Chicago market (-9.5 USD / tn), oil byproducts (-12 USD / tn) and flour (-4, USD 75 / tn). As discussed above, although a world reference price for soy is negotiated in Chicago, it does not indicate that prices in local markets move in the same way. In recent weeks there has been a strong pace of purchases from the industries, and by-prudoducts´ FOB export prices remained constant, supporting the payment capacity of the "oil industry". This is due to an increase in by-products´ export premiums that offset the drops in Chicago. Thus, since the beginning of June, soybeans in Chicago have been dropping approx. 67 USD / tn, while the industry's ability to pay fell approx. 38 USD / tn. Regarding the commercialization, the export and industrial sectors have purchased 24.6 Mt of the 2017/18 soybeans, equivalent to 70% of the total production. The pace of purchases remains far above previous years. It can be seen on the other hand that, despite the "closing of the North American market" for imports from China, Argentine soybean external sales have not accelerated in recent weeks. At the end of June, soybean export sales barely reached 1.29 Mt. The damage suffered by the local soybean harvest is evident, not only because of its volume, but also in terms of its quality.

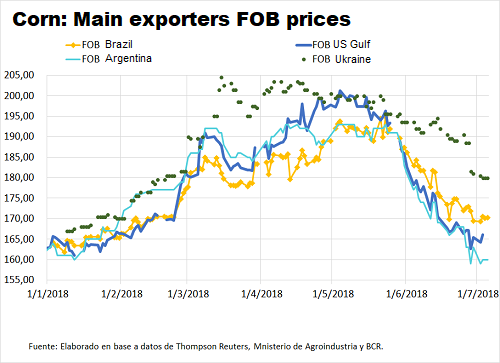

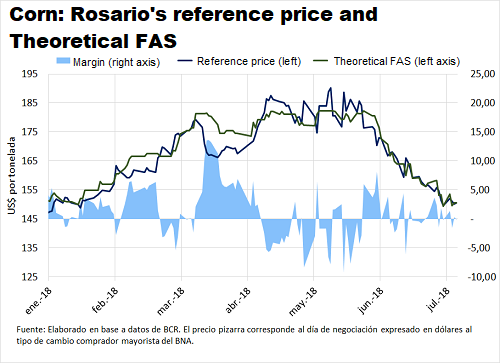

On the other hand, the price of local corn also fell sharply in the previous week. The reference price was equivalent to 150.6 USD / tn on Thursday July 5, noting a weekly fall of 0.80 USD / t. The fall in the price of corn in the last week is due to lower prices in foreign markets. The price of corn in the domestic market remains relatively stable in the last week, in the same way as FOB export prices. After a sharp fall in the month of June, the cereal price seems to be reaching a floor, due to the reduction in the Brazi's projected production. In addition, the strong indicators of US corn exports, discussed above, indicate that despite the trade conflict between China and the US, the demand for corn remains robust internationally.

On the other hand, the price of local corn also fell sharply in the previous week. The reference price was equivalent to 150.6 USD / tn on Thursday July 5, noting a weekly fall of 0.80 USD / t. The fall in the price of corn in the last week is due to lower prices in foreign markets. The price of corn in the domestic market remains relatively stable in the last week, in the same way as FOB export prices. After a sharp fall in the month of June, the cereal price seems to be reaching a floor, due to the reduction in the Brazi's projected production. In addition, the strong indicators of US corn exports, discussed above, indicate that despite the trade conflict between China and the US, the demand for corn remains robust internationally.