International low prices put pressure on soybeans, but the demand for export sustains corn

EMILCE TERRÉ

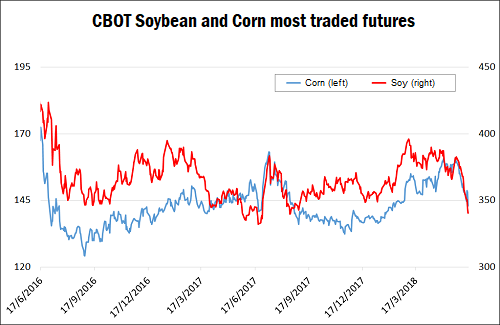

On Friday, the President of the United States, Donald Trump, provided news on his trade policy for imports from China, blowing the commodity markets. With China being the destination of more than 60% of US soybean exports, it is not surprising that the complicated outlook for the main American soybean buyer fully impacts on prices, as can be seen in the attached graph.

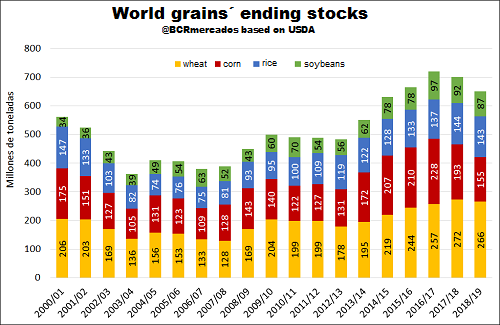

The commercial conflicts were more than a moderately bullish report from the United States Department of Agriculture (USDA), which in its monthly publication of estimates of supply and demand projected a US soybean processing for the current 2017/18 season that exceeded previous expectations. Higher industrial use would adjust the level of bean inventories, which usually correlates positively with prices. At a global level, meanwhile, there were no major changes to the forecasts of supply and demand of soybeans in the world, although it did increase the estimated production for Brazil to 119 million tons (2 Mt more than expected in May). , while the projected output for our country fell 2 million to 37 Mt. Regarding corn, the agency also adjusted stocks that would go from 2017/18 to 2018/19, based on higher exports from the United States. These are advancing at a much faster pace than they showed in previous campaigns for the same height of the year, as can be seen in the second graph. The world forecast of a more robust demand for ethanol production in the new 2018/19 commercial year had a high impact on the market, combined with a more adjusted supply (due to the lower production that Russia would obtain, mainly), would substantially reduce the ending stocks. Indeed, final stocks of the next crop year would barely cover 14% of the world's domestic corn consumption, the lowest percentage of the last 8 years. The third graph illustrates that the projection of a more adjusted supply scenario is shared by the crops that produce and demand the world the most. While already in the current 2017/18 commercial year, the lower South American production eroded global inventories of soybeans and corn, by 2018/19 not only would continue to cut the stock of these coarse grains but for the first time in six years the final wheat stock would fall. Overall, this forecast of an increase in international demand for grains above the expected increase in the supply, will act as a support for commodity prices for the next season.

The commercial conflicts were more than a moderately bullish report from the United States Department of Agriculture (USDA), which in its monthly publication of estimates of supply and demand projected a US soybean processing for the current 2017/18 season that exceeded previous expectations. Higher industrial use would adjust the level of bean inventories, which usually correlates positively with prices. At a global level, meanwhile, there were no major changes to the forecasts of supply and demand of soybeans in the world, although it did increase the estimated production for Brazil to 119 million tons (2 Mt more than expected in May). , while the projected output for our country fell 2 million to 37 Mt. Regarding corn, the agency also adjusted stocks that would go from 2017/18 to 2018/19, based on higher exports from the United States. These are advancing at a much faster pace than they showed in previous campaigns for the same height of the year, as can be seen in the second graph. The world forecast of a more robust demand for ethanol production in the new 2018/19 commercial year had a high impact on the market, combined with a more adjusted supply (due to the lower production that Russia would obtain, mainly), would substantially reduce the ending stocks. Indeed, final stocks of the next crop year would barely cover 14% of the world's domestic corn consumption, the lowest percentage of the last 8 years. The third graph illustrates that the projection of a more adjusted supply scenario is shared by the crops that produce and demand the world the most. While already in the current 2017/18 commercial year, the lower South American production eroded global inventories of soybeans and corn, by 2018/19 not only would continue to cut the stock of these coarse grains but for the first time in six years the final wheat stock would fall. Overall, this forecast of an increase in international demand for grains above the expected increase in the supply, will act as a support for commodity prices for the next season.

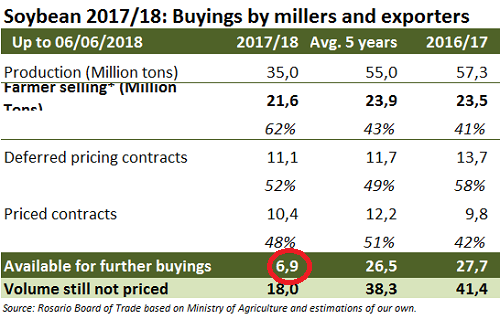

In the local market, the price of the oilseed increased on Thursday as a result of a rise in the exchange rate, although traders are being cautious in the middle of a very complicated productive campaign (it can be observed in the attached table that the volume remnant to commercialize for the remainder of 2017/2018 in relation to production is much lower than previous crop years), and also damaged by the external decline in prices. Rosario Board of Trade´s soybean reference prices rose AR$ 325 / t on Thursday, to AR$ 7,620 / t, up 6% on the week despite the fact that the variation in dollars is negative by 5%, according to the Argentine National Bank buyer's exchange rate.

In the local market, the price of the oilseed increased on Thursday as a result of a rise in the exchange rate, although traders are being cautious in the middle of a very complicated productive campaign (it can be observed in the attached table that the volume remnant to commercialize for the remainder of 2017/2018 in relation to production is much lower than previous crop years), and also damaged by the external decline in prices. Rosario Board of Trade´s soybean reference prices rose AR$ 325 / t on Thursday, to AR$ 7,620 / t, up 6% on the week despite the fact that the variation in dollars is negative by 5%, according to the Argentine National Bank buyer's exchange rate.

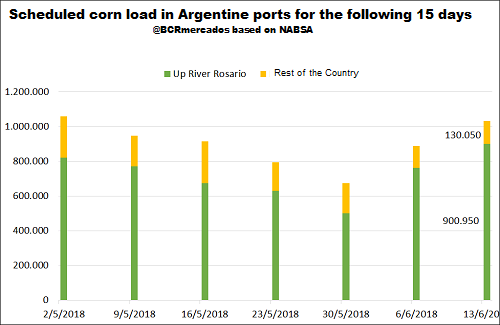

Corn, on the other hand, showed a strong volume of negotiations in the spot segment. The reference price for Thursday's operations was AR$ 4,480 / t, 8% above the reference price of the previous week, although in dollars it fell by 3% (using the Argentine National Bank's buyer exchange rate). Contrary, the prices offered for 2018/19 corn fell a step towards the end of the week, although there were a lot of negotiations. The need to receive merchandise in the short term by corn exporters in the area is based on the high volume of shipments scheduled for the coming weeks. According to the records of the maritime agency NABSA from the Up River port terminals, about one million tons would be dispatched, and another 130,000 tons from other ports.

Corn, on the other hand, showed a strong volume of negotiations in the spot segment. The reference price for Thursday's operations was AR$ 4,480 / t, 8% above the reference price of the previous week, although in dollars it fell by 3% (using the Argentine National Bank's buyer exchange rate). Contrary, the prices offered for 2018/19 corn fell a step towards the end of the week, although there were a lot of negotiations. The need to receive merchandise in the short term by corn exporters in the area is based on the high volume of shipments scheduled for the coming weeks. According to the records of the maritime agency NABSA from the Up River port terminals, about one million tons would be dispatched, and another 130,000 tons from other ports.