Good perspectives for 2018/19 wheat planting in Argentina

PATRICIA BERGERO - FEDERICO DI YENNO

The local wheat´s strong demand maintains good prospects for new crop's wheat prices. Furthermore, stocks are very limited, against a very strong export demand and local milling. The spot price of wheat rose importantly on the previous week in the Rosario Board of Trade. It started on Monday being negotiated at AR $ 5,250 / t, to reach on Thursday a maximum of AR $ 5,700 / t. The demand is very active in this segment. Taking the variation of the prices to a week, compared to Thursday May 3, the price of wheat rose 24 USD. On the other hand, the price of wheat for the next crop year suffered an important decline. Indeed, wheat with delivery in December had been traded in the week at values around 190 and 193 US dollars per ton, decreasing to U$S 185 / t on Thursday.

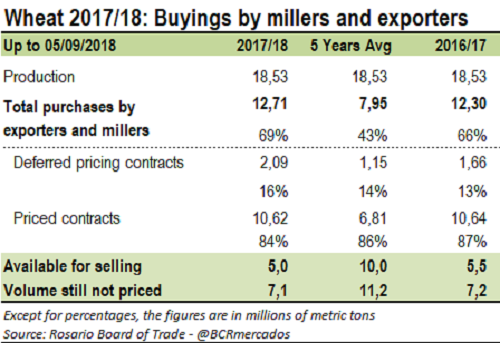

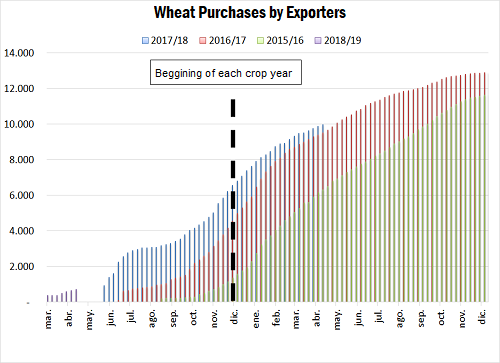

According to the Argentine Ministry of Agribusiness, millers and exporters had acquired 12.7 million tons of the cereal to May 2. This volume represents 73% of the 2017/18 wheat crop, which is estimated at 17.5 million tons. This ratio is above the 68% observed in the last marketing year and 66% of the average of the last five crop years. Analyzing by sector, millers' purchases remain very similar to previous years, while the volume purchased by the exporters, at this height of the year, exceeds the amount of the previous crop year even with lower production and, therefore, lower projected exports. In relation to the latter, companies have already bought 90% of the projected export for this year, while in the last marketing year that ratio amounted to 74%. The acceleration in the purchasing rhythm is also observed in the new 2018/19 harvest´s wheat, reaching the highest volume of forwards of the last 17 years.

According to the Argentine Ministry of Agribusiness, millers and exporters had acquired 12.7 million tons of the cereal to May 2. This volume represents 73% of the 2017/18 wheat crop, which is estimated at 17.5 million tons. This ratio is above the 68% observed in the last marketing year and 66% of the average of the last five crop years. Analyzing by sector, millers' purchases remain very similar to previous years, while the volume purchased by the exporters, at this height of the year, exceeds the amount of the previous crop year even with lower production and, therefore, lower projected exports. In relation to the latter, companies have already bought 90% of the projected export for this year, while in the last marketing year that ratio amounted to 74%. The acceleration in the purchasing rhythm is also observed in the new 2018/19 harvest´s wheat, reaching the highest volume of forwards of the last 17 years.

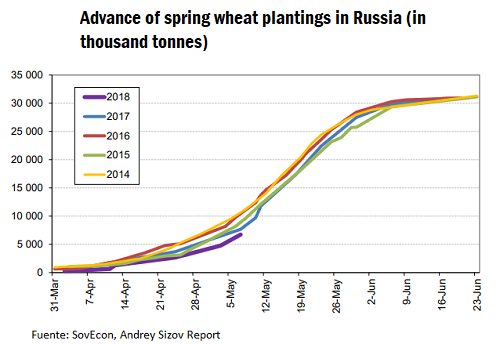

The strong demand for Argentine exports, plus the adjusted present stocks, has been reflected in the price of wheat in the domestic market. According to MATba (Buenos Aires Futures Market), a good part of the operations of wheat to harvest, delivery in December in Rosario, has been above the US $ 190 / t, registering a minimum of US $ 186 and a maximum of US $ 197 in the week. International Panorama The International Grains Council (CIG) affirmed that the 2018/19 crop year continues to point to a global wheat harvest lower than last season, although higher than the previous three marketing years. In general, a recession in the area sown with wheat on a global scale is foreseen - the third consecutive fall -, with the exception of the US and Argentina and possibly with very little variation in Canada, Ukraine and Australia -all countries within the main exporting producers-. The main reasons for productive uncertainty regarding are given by the US, Australia and Argentina. With a world production estimated at 739 Mt for 2018/19, for the first time since 2012/13 the figure would be falling below the level of consumption (745 Mt), which is an important figure due to the growth in human consumption, mainly in Asian and African countries. In the case of the US, although the planting intentions for 2018/19 pointed to an increase in area, the climate is affecting the possibility to plant spring wheat. The latest USDA report showed that 30% of this cereal was planted by May 6, compared to an average of 51% for the previous five seasons. In the case of winter wheat, there was 34% of the area under good to excellent conditions, compared to 53% last year. Rains occurred in parts of the southern US plains, but drought conditions persist in much of Kansas, Oklahoma and Texas, the major producing states of winter wheat. Currently, the world's largest wheat exporter, Russia, is carrying out the planting of spring wheat, which, according to projections by consultants from that country, would yield a very good production, in historical terms, even if it is below what was harvested in 2017/18. According to these same private sources, the Russian wheat crop could reach 78.2 million tons, taking into account the set of spring wheat and winter wheat crops. This volume would be lower than the 85.9 Mt last year due to a decrease in the planted area and the potential for lower yields due to the lower investment of the producers in terms of inputs (seeds, fertilizers, inoculants, etc.). The vision of the USDA aggregate in this country is different, and anticipates a production of 72 Mt by a combination of smaller area and yields slightly above the trend assuming the climatic conditions were normal. The same source anticipated an exportable balance of 36.5 Mt, slightly below the 38 Mt of 2017/18, considering that the remaining stocks would add volume to external sales, partially offsetting the lower production. This last figure is still very high, so the wheat market is closely following the evolution of this crop.

The strong demand for Argentine exports, plus the adjusted present stocks, has been reflected in the price of wheat in the domestic market. According to MATba (Buenos Aires Futures Market), a good part of the operations of wheat to harvest, delivery in December in Rosario, has been above the US $ 190 / t, registering a minimum of US $ 186 and a maximum of US $ 197 in the week. International Panorama The International Grains Council (CIG) affirmed that the 2018/19 crop year continues to point to a global wheat harvest lower than last season, although higher than the previous three marketing years. In general, a recession in the area sown with wheat on a global scale is foreseen - the third consecutive fall -, with the exception of the US and Argentina and possibly with very little variation in Canada, Ukraine and Australia -all countries within the main exporting producers-. The main reasons for productive uncertainty regarding are given by the US, Australia and Argentina. With a world production estimated at 739 Mt for 2018/19, for the first time since 2012/13 the figure would be falling below the level of consumption (745 Mt), which is an important figure due to the growth in human consumption, mainly in Asian and African countries. In the case of the US, although the planting intentions for 2018/19 pointed to an increase in area, the climate is affecting the possibility to plant spring wheat. The latest USDA report showed that 30% of this cereal was planted by May 6, compared to an average of 51% for the previous five seasons. In the case of winter wheat, there was 34% of the area under good to excellent conditions, compared to 53% last year. Rains occurred in parts of the southern US plains, but drought conditions persist in much of Kansas, Oklahoma and Texas, the major producing states of winter wheat. Currently, the world's largest wheat exporter, Russia, is carrying out the planting of spring wheat, which, according to projections by consultants from that country, would yield a very good production, in historical terms, even if it is below what was harvested in 2017/18. According to these same private sources, the Russian wheat crop could reach 78.2 million tons, taking into account the set of spring wheat and winter wheat crops. This volume would be lower than the 85.9 Mt last year due to a decrease in the planted area and the potential for lower yields due to the lower investment of the producers in terms of inputs (seeds, fertilizers, inoculants, etc.). The vision of the USDA aggregate in this country is different, and anticipates a production of 72 Mt by a combination of smaller area and yields slightly above the trend assuming the climatic conditions were normal. The same source anticipated an exportable balance of 36.5 Mt, slightly below the 38 Mt of 2017/18, considering that the remaining stocks would add volume to external sales, partially offsetting the lower production. This last figure is still very high, so the wheat market is closely following the evolution of this crop.

The weather also plays a very important role at this time since the Russian winter wheat is in development, so yields can be very different from those projected. On the other hand, in several wheat areas, the progress of planting is very slow compared to other years, and rains are needed for the next 15 days to improve the state of winter wheat. This phenomenon will determine if the production projections will be adjusted downwards or will remain the same, which constitutes a fundamental factor for cereal prices in international markets.

The weather also plays a very important role at this time since the Russian winter wheat is in development, so yields can be very different from those projected. On the other hand, in several wheat areas, the progress of planting is very slow compared to other years, and rains are needed for the next 15 days to improve the state of winter wheat. This phenomenon will determine if the production projections will be adjusted downwards or will remain the same, which constitutes a fundamental factor for cereal prices in international markets.