The external demand of 2018/19 wheat increases, but also the exports of competing countries

SOFÍA CORINA - FEDERICO DI YENNO

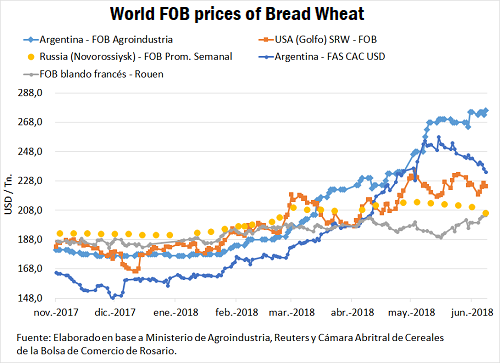

The price of spot wheat lost 21 dollars in the last week The prices of wheat registered in the Rosario Board of Trade, which continued its downward trend, fell sharply compared to the previous week in the spot segment measured in dollars. Although the reference price increased from $ 5,880 / t on Thursday June 7 to $ 6,000 / t on Thursday 14, in American dollars, the price decreased from U$S 236 / t on Thursday 7 to 217,4 / t on Thursday 14, more than 21 USD / t. If we count from Thursday, May 31, the price is falling 26 USD and more than 40 USD from the maximum reached on May 15 this year. The volume traded in the week also decreased compared to that negotiated in the previous week. According to official data, what was negotiated between Friday 8 and Thursday 14 with immediate delivery was almost zero, just 420 tons. Compared with local FOB prices, which remained unchanged, the local price for spot wheat had a significant decline.

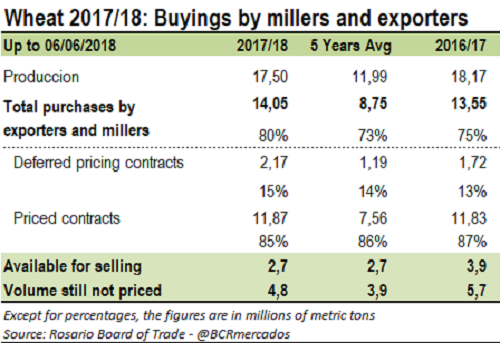

2017/18 marketing already reaches 80% of the harvest The fall in wheat prices follows the knowledge of robust marketing indicators that mark 80% of the wheat crop traded as of June 6. Taking into account the difference between the 2017/18 External Sales of the export sector and the declared purchases, more, the purchases minus the processed volume by the miller sector, as of June 6, both sectors would only hold inventories for 600 thousand tons. This is, always taking into account the external sales by the export sector of 10.56 Mt. If we take to date the estimated shipments of 8.96 Mt (Dec to June 06, do not count the exported in November that could come from the 17/18 harvest of wheat) the remaining stock of both sectors reaches 2.23 Mt.

2017/18 marketing already reaches 80% of the harvest The fall in wheat prices follows the knowledge of robust marketing indicators that mark 80% of the wheat crop traded as of June 6. Taking into account the difference between the 2017/18 External Sales of the export sector and the declared purchases, more, the purchases minus the processed volume by the miller sector, as of June 6, both sectors would only hold inventories for 600 thousand tons. This is, always taking into account the external sales by the export sector of 10.56 Mt. If we take to date the estimated shipments of 8.96 Mt (Dec to June 06, do not count the exported in November that could come from the 17/18 harvest of wheat) the remaining stock of both sectors reaches 2.23 Mt.

The commercialization of next harvest wheat is one of the highest on record The commercialization of wheat to harvest reaches 2.1 Mt to June 6 of the current year. The tonnage of forwards negotiated to harvest is only comparable with the 2001/02 commercial year. During the week, the volume traded of wheat 18/19 increased by 380 thousand tons. The accelerated pace of commercialization is also seen in export sales. As of June 6, external sales reached 1.73 Mt, being to date the highest value on record.

The commercialization of next harvest wheat is one of the highest on record The commercialization of wheat to harvest reaches 2.1 Mt to June 6 of the current year. The tonnage of forwards negotiated to harvest is only comparable with the 2001/02 commercial year. During the week, the volume traded of wheat 18/19 increased by 380 thousand tons. The accelerated pace of commercialization is also seen in export sales. As of June 6, external sales reached 1.73 Mt, being to date the highest value on record.

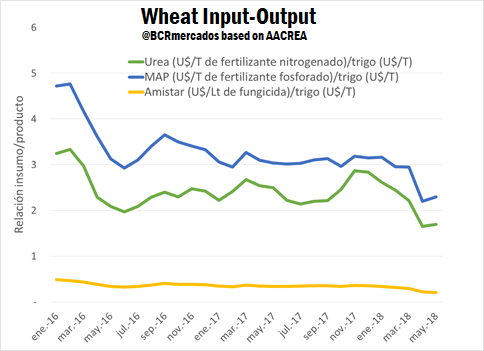

Technology developments Wheat sowing advances in the core region covering 48% of the area, according to our institution's Strategic Guide for Agriculture, while the technology used points to good yields at a country level. In this line, the input-output ratio is one of the main triggers of investment in input technology. The following graph shows how the ratio of the price of some main inputs to the price of wheat considerably decreased since the end of 2017.

Technology developments Wheat sowing advances in the core region covering 48% of the area, according to our institution's Strategic Guide for Agriculture, while the technology used points to good yields at a country level. In this line, the input-output ratio is one of the main triggers of investment in input technology. The following graph shows how the ratio of the price of some main inputs to the price of wheat considerably decreased since the end of 2017.

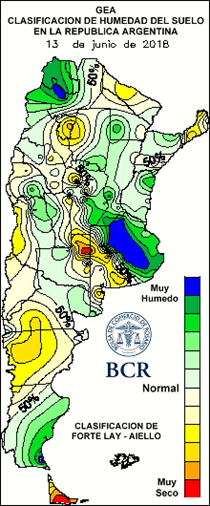

Regarding the soil´s humidity for wheat sowing, the following map shows a marked difference between the east and west of the country. The north of Buenos Aires presents conditions of excess humidity while, part of Córdoba, west of Buenos Aires and La Pampa, the reserves become deficient. Despite this, long cycles are being planted and many producers started with the introduction of intermediate cycles.

Regarding the soil´s humidity for wheat sowing, the following map shows a marked difference between the east and west of the country. The north of Buenos Aires presents conditions of excess humidity while, part of Córdoba, west of Buenos Aires and La Pampa, the reserves become deficient. Despite this, long cycles are being planted and many producers started with the introduction of intermediate cycles.

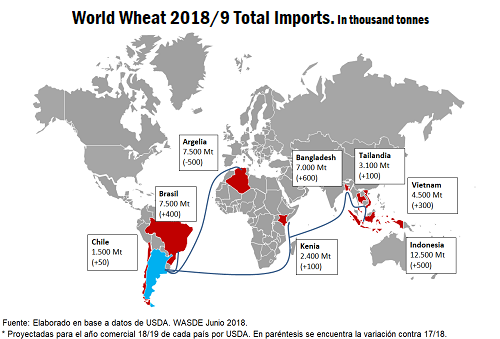

Countries such as Kenya and Indonesia would sustain the external demand of Argentine wheat According to the latest USDA report, Southeast Asia and Sub-Saharan Africa are forecast to be the two largest wheat importing regions in the world after continued growth over the past decade. Both regions have developed a greater taste for diets that include more wheat, which has been driving demand for imports. The rapid growth of imports in Southeast Asia has also been driven by increased use of wheat in food rations, while the growth of sub-Saharan Africa is based mainly on rapid population growth and urbanization. Historically, North Africa and the Middle East were the most relevant regions for world wheat imports. However, in the last decade, consumption in those regions has not grown as fast as in Southeast Asia and sub-Saharan Africa. Specifically in 2018/19, it is forecast that both North Africa and the Middle East will have lower wheat imports due to the abundant harvests in the main importing countries. North African imports are expected to fall due to higher production in Algeria, Morocco and Tunisia. Imports from the Middle East are forecast to be lower due to the fact that Turkey's lower demand is expected to offset imports elsewhere.

Countries such as Kenya and Indonesia would sustain the external demand of Argentine wheat According to the latest USDA report, Southeast Asia and Sub-Saharan Africa are forecast to be the two largest wheat importing regions in the world after continued growth over the past decade. Both regions have developed a greater taste for diets that include more wheat, which has been driving demand for imports. The rapid growth of imports in Southeast Asia has also been driven by increased use of wheat in food rations, while the growth of sub-Saharan Africa is based mainly on rapid population growth and urbanization. Historically, North Africa and the Middle East were the most relevant regions for world wheat imports. However, in the last decade, consumption in those regions has not grown as fast as in Southeast Asia and sub-Saharan Africa. Specifically in 2018/19, it is forecast that both North Africa and the Middle East will have lower wheat imports due to the abundant harvests in the main importing countries. North African imports are expected to fall due to higher production in Algeria, Morocco and Tunisia. Imports from the Middle East are forecast to be lower due to the fact that Turkey's lower demand is expected to offset imports elsewhere.

Argentina's wheat has a lot to gain considering the higher production volume projected for the next local season and the expected increase in external demand for the same period. It is expected that Argentina's main wheat importers increase their total imports in the period 18/19 by 1.55 Mt. Much of this increase will come from destinations outside of South America with an increase of 1.15 Mt. However, the stimulus of demand for Argentine wheat may be undermined by higher exports from competitors such as Australia and Canada in the new 18/19 season. Australia has a harvest calendar (Oct-Sept, the national calendar is Dec-Nov) similar to Argentina for finding us in similar latitudes. Australia is expected to produce 21.9 million tonnes of wheat in 2018/19 (October-September), 3% more than the 21.2 million tonnes in the previous season, despite a slight decrease in the surface due to the limited planting intention due to dry weather, according to the report of the Australian Bureau of Economics and Agricultural Sciences and Resources (ABARES) on June crops published Tuesday night. The estimates of ABARES suppose a timely and sufficient winter precipitation, particularly in areas where there is common below-average winter rainfall. Australia experienced the third heaviest registered May and June is likely to be drier than average in much of the country, according to the Bureau of Meteorology. Globally, despite a lower production of Russian wheat, and consequently, lower exports; the overall balance is still adjusted, even with stocks on the rise. The USDA in its latest Supply and Demand report, increased the final stocks of the 18/19 commercial year by 1.8 Mt. Despite lower production (it comes from the Russian cut of 3.5 Mt) a lower demand is projected international trade and less grain trade for that period.

Argentina's wheat has a lot to gain considering the higher production volume projected for the next local season and the expected increase in external demand for the same period. It is expected that Argentina's main wheat importers increase their total imports in the period 18/19 by 1.55 Mt. Much of this increase will come from destinations outside of South America with an increase of 1.15 Mt. However, the stimulus of demand for Argentine wheat may be undermined by higher exports from competitors such as Australia and Canada in the new 18/19 season. Australia has a harvest calendar (Oct-Sept, the national calendar is Dec-Nov) similar to Argentina for finding us in similar latitudes. Australia is expected to produce 21.9 million tonnes of wheat in 2018/19 (October-September), 3% more than the 21.2 million tonnes in the previous season, despite a slight decrease in the surface due to the limited planting intention due to dry weather, according to the report of the Australian Bureau of Economics and Agricultural Sciences and Resources (ABARES) on June crops published Tuesday night. The estimates of ABARES suppose a timely and sufficient winter precipitation, particularly in areas where there is common below-average winter rainfall. Australia experienced the third heaviest registered May and June is likely to be drier than average in much of the country, according to the Bureau of Meteorology. Globally, despite a lower production of Russian wheat, and consequently, lower exports; the overall balance is still adjusted, even with stocks on the rise. The USDA in its latest Supply and Demand report, increased the final stocks of the 18/19 commercial year by 1.8 Mt. Despite lower production (it comes from the Russian cut of 3.5 Mt) a lower demand is projected international trade and less grain trade for that period.