Having fulfilled the merchandise origination needs to meet current commitments, the export sector took pressure off the wheat market, causing prices to deflate. For the current 2017/18 commercial year, the export commitments amount to 10.8 Mt, while the purchases accumulated by the exporters total 11 Mt. The available supply also makes it practically impossible for the total volume dispatched abroad to exceed that amount without neglecting the needs of domestic consumption. In relation to the new 2018/19 crop year, the export commitments of the export sector register an unprecedented volume of 2.46 Mt, while the sector's purchases amounted to 2.38 Mt on June 13.

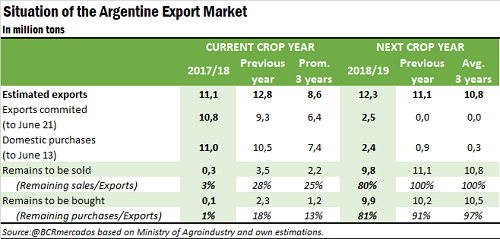

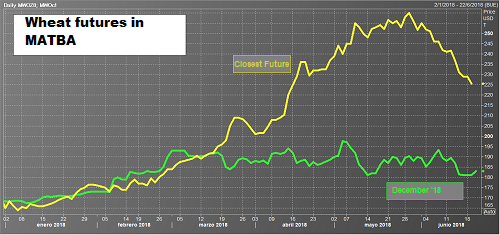

As shown in the attached table, both what remains to be sold (9.8 Mt) and what remains to be purchased, based on current export estimates (9.9 Mt), are well below what was recorded at the same height of the previous year as well as the average of the last three years, both for the current and the following commercial years. Of the 2017/18 crop year, only 300,000 tons remain to be sold by June 21, although based on the level of inventories in the export sector, only the purchase of less than 100,000 tons by mid-June remained. At the same date last year, there were still 3.5 Mt left and 2.3 Mt, while in the last three years these volumes were 2.2 and 1.2 Mt, respectively. For the new 2018/19 crop year, the high volume of export commitments stands out (2.5 Mt), when by June of the last three years no export contract had yet been made. In order to meet these commitments, exporters had acquired 2.4 million tons in mid-June. In this context, despite the expected recovery in wheat exports for next year, the percentage of merchandise that remains to be bought and sold by the export sector is significantly lower than in previous years. Thus, the number of active buyers in the local wheat market was significantly reduced over the last weeks. Along with the lower pressure of export demand, cereal prices deflated, especially in the spot segment. The Rosario Board of Trade´s reference price for last Thursday's operations was AR$ 5,920 / t, AR$ 80 / t below the previous week, while the nearest contract negotiated in MATBA (Buenos Aires Futures Market) closed on US $ 223 / t, with a weekly fall of 1.3%, as shown in the attached graph.

As shown in the attached table, both what remains to be sold (9.8 Mt) and what remains to be purchased, based on current export estimates (9.9 Mt), are well below what was recorded at the same height of the previous year as well as the average of the last three years, both for the current and the following commercial years. Of the 2017/18 crop year, only 300,000 tons remain to be sold by June 21, although based on the level of inventories in the export sector, only the purchase of less than 100,000 tons by mid-June remained. At the same date last year, there were still 3.5 Mt left and 2.3 Mt, while in the last three years these volumes were 2.2 and 1.2 Mt, respectively. For the new 2018/19 crop year, the high volume of export commitments stands out (2.5 Mt), when by June of the last three years no export contract had yet been made. In order to meet these commitments, exporters had acquired 2.4 million tons in mid-June. In this context, despite the expected recovery in wheat exports for next year, the percentage of merchandise that remains to be bought and sold by the export sector is significantly lower than in previous years. Thus, the number of active buyers in the local wheat market was significantly reduced over the last weeks. Along with the lower pressure of export demand, cereal prices deflated, especially in the spot segment. The Rosario Board of Trade´s reference price for last Thursday's operations was AR$ 5,920 / t, AR$ 80 / t below the previous week, while the nearest contract negotiated in MATBA (Buenos Aires Futures Market) closed on US $ 223 / t, with a weekly fall of 1.3%, as shown in the attached graph.

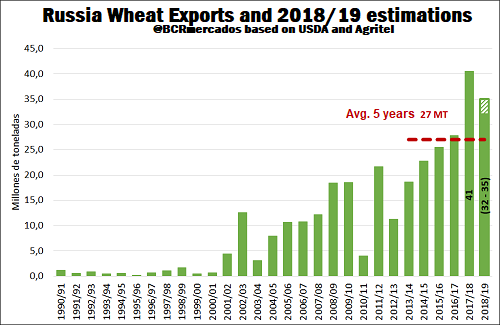

The prices of futures for the new harvest, in December 2018, were supported on last Thursday by the international wheat context. Russian production has been suffering from the adverse weather, improving the export prospects of the rest of the international cereal suppliers. Meanwhile, the Ministry of Agroindustry reported in the week that, of a total area to be planted that is officially estimated at 6,135 million hectares, already 33% of the total has been covered. That is slightly below the 35% of last year, although in general terms the good humidity conditions that characterize the development of the plantations stand out. In the international arena, wheat began to recover in the Chicago market after losing US$ 27 / tonne since the end of May, affected by seasonal pressure generated by the advance of crops in North America. This recovery is mainly due to climatic adversities that affect the Russian wheat production. In this regard, the French agency Agritel expects the host of the 2018 World Cup to see its 2018/19 wheat production drop to 67.4 MT, 21.5% lower than last season. This is due to two combined factors: on the one hand, the dry climate and high temperatures that affected winter wheat, and, on the other hand, excessive rains, mainly in Siberia, which delayed summer wheat plantings. In this context, the agency expects cereal exports to fall to the range of 32 to 34 million tons, below the 35 Mt projected by the USDA in its monthly report. This volume is much lower than the shipments of the previous year, although it would still be higher than the average of the last 5 years, as shown in the attached graph.

The prices of futures for the new harvest, in December 2018, were supported on last Thursday by the international wheat context. Russian production has been suffering from the adverse weather, improving the export prospects of the rest of the international cereal suppliers. Meanwhile, the Ministry of Agroindustry reported in the week that, of a total area to be planted that is officially estimated at 6,135 million hectares, already 33% of the total has been covered. That is slightly below the 35% of last year, although in general terms the good humidity conditions that characterize the development of the plantations stand out. In the international arena, wheat began to recover in the Chicago market after losing US$ 27 / tonne since the end of May, affected by seasonal pressure generated by the advance of crops in North America. This recovery is mainly due to climatic adversities that affect the Russian wheat production. In this regard, the French agency Agritel expects the host of the 2018 World Cup to see its 2018/19 wheat production drop to 67.4 MT, 21.5% lower than last season. This is due to two combined factors: on the one hand, the dry climate and high temperatures that affected winter wheat, and, on the other hand, excessive rains, mainly in Siberia, which delayed summer wheat plantings. In this context, the agency expects cereal exports to fall to the range of 32 to 34 million tons, below the 35 Mt projected by the USDA in its monthly report. This volume is much lower than the shipments of the previous year, although it would still be higher than the average of the last 5 years, as shown in the attached graph.

Another country that is also being affected by adverse weather conditions is China, the world's leading cereal producer and consumer. According to the agency Thomson Reuters, its production of this grain could fall up to 20% in 2018. This could boost imports from the Asian country, which exerts a greater upward influence on prices. Given the commercial conflict that hinders the exchange between the United States and China, the main beneficiaries of this situation, by a geographical issue, would be Canada and the countries of the Black Sea region, although its spillover effect will be felt in all the suppliers of the world, including Argentina.

Another country that is also being affected by adverse weather conditions is China, the world's leading cereal producer and consumer. According to the agency Thomson Reuters, its production of this grain could fall up to 20% in 2018. This could boost imports from the Asian country, which exerts a greater upward influence on prices. Given the commercial conflict that hinders the exchange between the United States and China, the main beneficiaries of this situation, by a geographical issue, would be Canada and the countries of the Black Sea region, although its spillover effect will be felt in all the suppliers of the world, including Argentina.