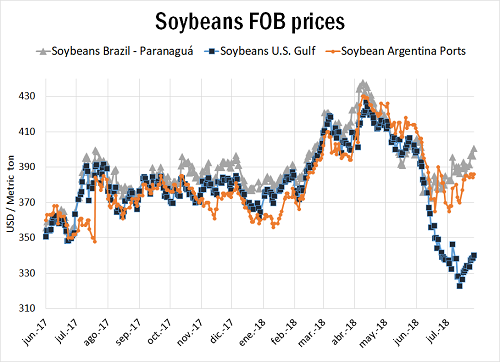

The situation at the wheat market around the world generated an upward pressure on the overall grains prices. The shortage on key wheat supplier countries supported the domestic prices of coarse grains in Argentina allowing a strong recovery in corn cash prices and a small (but milder) recovery in soybean deferred prices so far this week. In the week, the price of soybean published by the CAC (Arbitration Chamber of Cereals) of the BCR, was of 278.3 USD / t on Thursday July 26, remaining unchanged with respect to the value of Thursday July 19. The price for the local oilseed did not have the same upward momentum that it received in the reference market of Chicago, where it increased 5.6 USD / tn in the same period of time. The jump in the price of the oilseed at the US Market was driven by expectations of higher exports to Europe after the trade talks between Washington and the European Union, coupled with announcements of implementation of subsidies to US farmers seeking to correct the damages resulting from the commercial war with China.

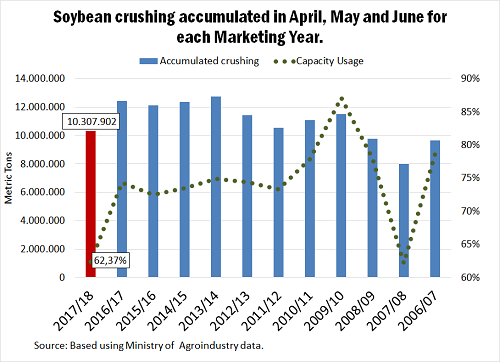

At the local level, in spite of the strong purchasing pace that the industrial sector carries in the 17/18 marketing year, the reported level of processed soybeans by the plants remains in sharp decline year to date. The accumulated soybean processing in the months of April, May and June of the 17/18 MY is the lowest in 9 years, reaching 10.3 million tons (Mt), showing a year to year decrease of 17%. A worrying figure for the sector is the use of installed capacity that reaches 62.4% of the theoretical maximum level (24 hours of processing per day), being the lowest since the first three months of the 2007/08 marketing year.

At the local level, in spite of the strong purchasing pace that the industrial sector carries in the 17/18 marketing year, the reported level of processed soybeans by the plants remains in sharp decline year to date. The accumulated soybean processing in the months of April, May and June of the 17/18 MY is the lowest in 9 years, reaching 10.3 million tons (Mt), showing a year to year decrease of 17%. A worrying figure for the sector is the use of installed capacity that reaches 62.4% of the theoretical maximum level (24 hours of processing per day), being the lowest since the first three months of the 2007/08 marketing year.

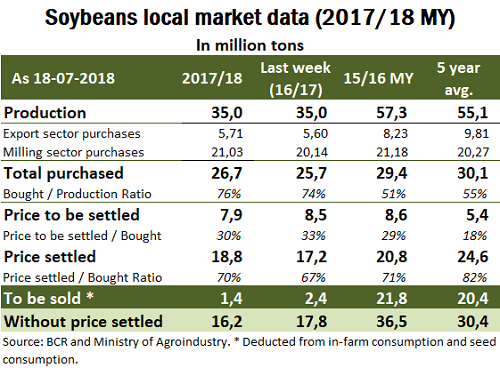

In the same sense, soybean meal export sales for 17/18 MY year to date, are far behind of other years. The total of 11.96 Mt is the lowest since the 12/13 MY. If there is no sudden change in the pattern of the soymeal trading, during the 17/18 TY, up to 4 million tons less of soybean meal would be exported compared with the previous season. The soybean meal export estimate in the 17/18 campaign of 25.5 Mt would indicate a total of 36 million tons of local soybean crushing, since there is an almost perfect correlation between soybean crushing and soymeal exports. When it comes to crushing and export positions at cash market, both sectors have already purchased a big quantity of stocks compared to the crushing expectations for the rest of the year. As of July 18, both sectors have acquired 76% of the soybean crop, while the high percentage of operations with prices to be set (30% of total operations) stands out. The soybean export sector maintains 4.31 Mt of acquired tons still not sold, while the industrial sector has a total of 8.63 Mt, still unprocessed. Together, both sectors have 12.9 Mt of soybeans to June 18, being well above what was estimated at the same date of the last marketing year. This yields bearish fundamentals for the price of local soybeans, if the forecasts of lower exports and processing compared to the previous year continues throughout the year.

In the same sense, soybean meal export sales for 17/18 MY year to date, are far behind of other years. The total of 11.96 Mt is the lowest since the 12/13 MY. If there is no sudden change in the pattern of the soymeal trading, during the 17/18 TY, up to 4 million tons less of soybean meal would be exported compared with the previous season. The soybean meal export estimate in the 17/18 campaign of 25.5 Mt would indicate a total of 36 million tons of local soybean crushing, since there is an almost perfect correlation between soybean crushing and soymeal exports. When it comes to crushing and export positions at cash market, both sectors have already purchased a big quantity of stocks compared to the crushing expectations for the rest of the year. As of July 18, both sectors have acquired 76% of the soybean crop, while the high percentage of operations with prices to be set (30% of total operations) stands out. The soybean export sector maintains 4.31 Mt of acquired tons still not sold, while the industrial sector has a total of 8.63 Mt, still unprocessed. Together, both sectors have 12.9 Mt of soybeans to June 18, being well above what was estimated at the same date of the last marketing year. This yields bearish fundamentals for the price of local soybeans, if the forecasts of lower exports and processing compared to the previous year continues throughout the year.

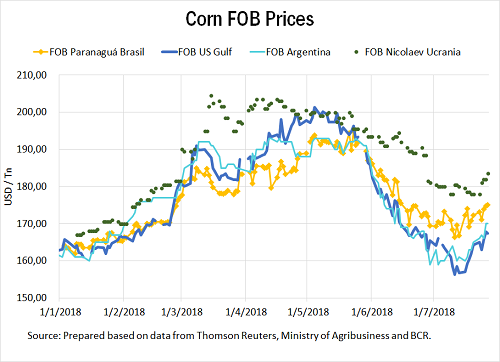

Corn rebounds in the week In the last week, the price of corn revealed by the CAC (Arbitration Chamber of Cereals) of the BCR, was of 162 USD / t on Thursday July 26, noting a recovery of 6.56 USD / t compared to Thursday 19 of July.

Corn rebounds in the week In the last week, the price of corn revealed by the CAC (Arbitration Chamber of Cereals) of the BCR, was of 162 USD / t on Thursday July 26, noting a recovery of 6.56 USD / t compared to Thursday 19 of July.

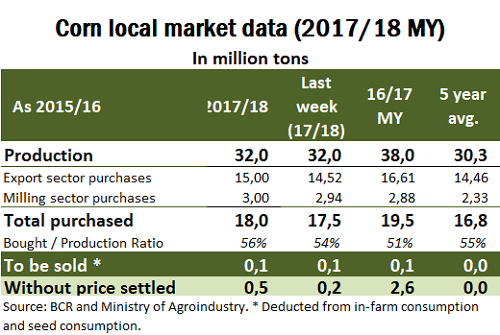

During the week, corn was able to make a profit mainly following the price of wheat, after knowing the production data of the main suppliers in the world: Russia, Ukraine, Europe, among others. In the note on wheat of the last weekly news we commented that several countries of great importance in the production and international trade of wheat were suffering hot and extremely dry weather conditions, which have put in check their prospects of production with an upward impact on the price of cereal in almost all markets. On the other hand, uncertainty about the possible impact of climatic conditions on the development of coarse grain crops in the Midwest of the United States also provided additional support to prices. It will be necessary to see in the coming days how the climatic variable evolves in these countries to know if this trend in prices is consolidated. With respect to the local level, corn purchases continue to put strong pressure on the domestic market. As of June 18, the purchases of the export sector exceed 15 million tons while the exports sales had very similar numbers which differs from the scenario seen in the soybean market. In this way, the fundamentals of the cereal end up being more robust than those of the oilseed.

During the week, corn was able to make a profit mainly following the price of wheat, after knowing the production data of the main suppliers in the world: Russia, Ukraine, Europe, among others. In the note on wheat of the last weekly news we commented that several countries of great importance in the production and international trade of wheat were suffering hot and extremely dry weather conditions, which have put in check their prospects of production with an upward impact on the price of cereal in almost all markets. On the other hand, uncertainty about the possible impact of climatic conditions on the development of coarse grain crops in the Midwest of the United States also provided additional support to prices. It will be necessary to see in the coming days how the climatic variable evolves in these countries to know if this trend in prices is consolidated. With respect to the local level, corn purchases continue to put strong pressure on the domestic market. As of June 18, the purchases of the export sector exceed 15 million tons while the exports sales had very similar numbers which differs from the scenario seen in the soybean market. In this way, the fundamentals of the cereal end up being more robust than those of the oilseed.