The commercial conflict between the US and China puts the price of coarse grains in suspense

FEDERICO DI YENNO

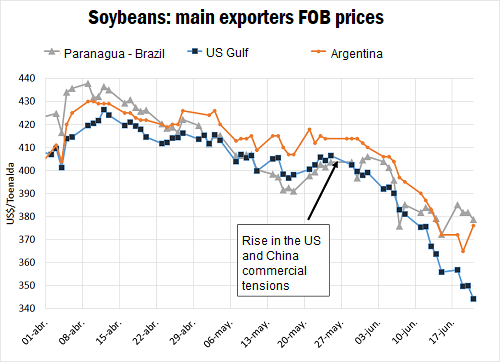

Argentine soybeans in the FOB markets lost USD 64 / t from the April highs after the tension in the trade dispute between the United States and China increased. A key fact to understand the importance of this conflict is what both powers represent: they hold 40% of the global GDP. According to US data, in 2017 China imported USD 129,890 million in goods from the United States, while the United States imported 505.47 billion USD in Chinese products. Therefore, the bilateral deficit of the North American country reached 375,000 million dollars. The commercial tension between both nations escalated on Friday 15 after the government of the United States revealed a list of products imported from China subject to revision of tariffs, which would reach an import value of 50,000 million dollars (M USD). The Trump Administration submitted a list of more than 800 strategically important import products from China that could be subject to a 25% tariff from July 6 (the list includes automobiles, among other products). This action from the US Administration comes after several meetings held by officials from Washington and Beijing. Additionally, the White House would announce the application of restrictions on investments by Chinese companies in the US as of June 30. The reports of market operators, and various media, already discounted these measures so the decline in soybeans in Chicago began before the announcement. The fall in soybean prices was not only discounting the measures of the Trump Administration, but also the possible retaliation of China.

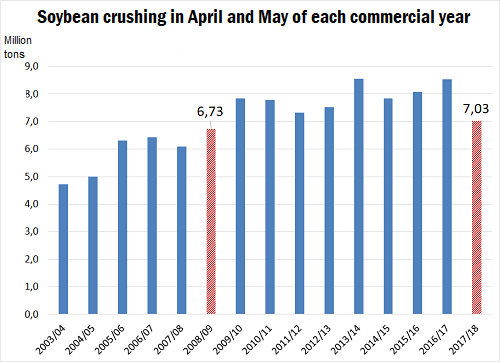

The Asian giant's counterattack was not long in coming when, on the same day, the Chinese Ministry of Commerce announced that they would impose tariffs "with the same reciprocity and scale" and that any prior agreement with the Trump Administration would be invalid. China's official news agency reported that China would impose tariffs of 25% on imports of 659 US products. The total would amount to 50,000 million dollars, including bean, soybeans and seafood-fish, among other products. The US agricultural products of that list, for 34,000 M USD, would be the most affected by the tariffs that would be effective as of July 6, the same date as in the US. It is recalled once again that soybean is the main product imported into China from the United States. China's list of products would have already increased six times from the list known in April; even so, the total amount of 50,000 million dollars would remain intact since imports of commercial aircraft would not be affected. On Monday 18, the US authorities in retaliation for the measures defined by the Asian country announced again a possible initiative to review tariffs on products imported from China, in addition to the previous ones . This initiative to impose tariffs would reach imported products from that country for an aggregate value of 200,000 million dollars, while the tariff would be 10%. China, in retribution, announced that it would apply other quantitative and qualitative measures if the United States publishes an additional list of Chinese products subject to tariffs. The United States government trade area, United States Trade Representative (USTR), indicated that the list of tariffs on the proposed products is being prepared, which would lead to a legal process similar to the previous ones, since the Proposals must undergo a period of public hearings and reviews. The commercialization of grains also received another blow on Monday 18, as Mexico could impose commercial measures to the 4,000 million dollars in annual imports of corn and soybeans from the United States if the government increases the escalation in the trade dispute with new tariffs. The price of soybeans suffered an even stronger drop on Tuesday, 19. The price of soybean futures traded in Chicago fell USD 24 / t in the middle of the day, touching December 2007 lows in the spot markets. This came after President Donald Trump again threatened tariffs on another 200,000 M USD of Chinese products should Beijing re-impose trade measures, which would raise to 450,000 M USD the potential quantity of Chinese exports that could fall below duty. This sum is close to USD 500,000 million in total annual Chinese exports to the United States. The outcome of this conflict is unpredictable and could seriously damage the world economy. The uncertainty generated, in and of itself, strongly affected the commodity and financial markets in general. In terms of international logistics, China's lower demand for the US bean is derived to Brazilian ports. The greater demand for the soya bean in that country increased the FOB price of the oilseed in the port of Paranaguá sharply, observing a spread of USD34 / t with the price of US soybeans. Argentina, in a mid-point, also accumulates better prices, but below Brazil. Activity of the local corn and soybean markets In the week, the Rosario Board of Trade´s reference price of soybeans, was of 276 USD / t on Thursday 21, marking a recovery of 1.83 USD / t with respect to Thursday 14. In spite of the slight recovery in the week, the price of local soybeans has maintained a bearish trend so far this June, due to the weakness in external prices discussed above. According to its crushing needs, the purchases of the industry mark a good rhythm to June 13, accumulating a total of 17.64 Mt, being a value very similar to what was acquired last season. Despite the good pace of purchases, processing in May, at 3.66 Mt, was much lower than in previous years. The cumulative crushing in the months of April and May is the lowest since 2008/2009, adding a little more than 7 million tons, product of the local drought, and despite an increase in soybean imports in the current season. The combined soybean imports in the months of April and May reach 1.14 Mt.

The Asian giant's counterattack was not long in coming when, on the same day, the Chinese Ministry of Commerce announced that they would impose tariffs "with the same reciprocity and scale" and that any prior agreement with the Trump Administration would be invalid. China's official news agency reported that China would impose tariffs of 25% on imports of 659 US products. The total would amount to 50,000 million dollars, including bean, soybeans and seafood-fish, among other products. The US agricultural products of that list, for 34,000 M USD, would be the most affected by the tariffs that would be effective as of July 6, the same date as in the US. It is recalled once again that soybean is the main product imported into China from the United States. China's list of products would have already increased six times from the list known in April; even so, the total amount of 50,000 million dollars would remain intact since imports of commercial aircraft would not be affected. On Monday 18, the US authorities in retaliation for the measures defined by the Asian country announced again a possible initiative to review tariffs on products imported from China, in addition to the previous ones . This initiative to impose tariffs would reach imported products from that country for an aggregate value of 200,000 million dollars, while the tariff would be 10%. China, in retribution, announced that it would apply other quantitative and qualitative measures if the United States publishes an additional list of Chinese products subject to tariffs. The United States government trade area, United States Trade Representative (USTR), indicated that the list of tariffs on the proposed products is being prepared, which would lead to a legal process similar to the previous ones, since the Proposals must undergo a period of public hearings and reviews. The commercialization of grains also received another blow on Monday 18, as Mexico could impose commercial measures to the 4,000 million dollars in annual imports of corn and soybeans from the United States if the government increases the escalation in the trade dispute with new tariffs. The price of soybeans suffered an even stronger drop on Tuesday, 19. The price of soybean futures traded in Chicago fell USD 24 / t in the middle of the day, touching December 2007 lows in the spot markets. This came after President Donald Trump again threatened tariffs on another 200,000 M USD of Chinese products should Beijing re-impose trade measures, which would raise to 450,000 M USD the potential quantity of Chinese exports that could fall below duty. This sum is close to USD 500,000 million in total annual Chinese exports to the United States. The outcome of this conflict is unpredictable and could seriously damage the world economy. The uncertainty generated, in and of itself, strongly affected the commodity and financial markets in general. In terms of international logistics, China's lower demand for the US bean is derived to Brazilian ports. The greater demand for the soya bean in that country increased the FOB price of the oilseed in the port of Paranaguá sharply, observing a spread of USD34 / t with the price of US soybeans. Argentina, in a mid-point, also accumulates better prices, but below Brazil. Activity of the local corn and soybean markets In the week, the Rosario Board of Trade´s reference price of soybeans, was of 276 USD / t on Thursday 21, marking a recovery of 1.83 USD / t with respect to Thursday 14. In spite of the slight recovery in the week, the price of local soybeans has maintained a bearish trend so far this June, due to the weakness in external prices discussed above. According to its crushing needs, the purchases of the industry mark a good rhythm to June 13, accumulating a total of 17.64 Mt, being a value very similar to what was acquired last season. Despite the good pace of purchases, processing in May, at 3.66 Mt, was much lower than in previous years. The cumulative crushing in the months of April and May is the lowest since 2008/2009, adding a little more than 7 million tons, product of the local drought, and despite an increase in soybean imports in the current season. The combined soybean imports in the months of April and May reach 1.14 Mt.

During the week, a smaller commercialized volume of soybean was registered compared to the previous week (taking into account one less trading day in the week). According to official data, 41 thousand tons were negotiated with immediate delivery in the week of Friday 8 to Thursday 14. In the week of Friday 15 to Thursday 21 the negotiated tonnage reached 26 thousand tons. With the same trend, the negotiated by delivery in July was also lower than last week (108 thousand tons, against 320 thousand tons). 30% of what was negotiated was made to fix price, 24% was negotiated at AR$ 7,700 / t mainly on Friday 15 and another similar percentage on the AR$ 7600 / t. Regarding the forward segment, an important tonnage negotiated on the month of October (96 thousand tons) is observed. On Friday 15, close to 35 thousand tons were closed at AR$ 8,200 / t for delivery until that month, while the rest of the week, they closed forwards for 52 thousand tons at AR$ 8,000 / t. A lower amount was negotiated for delivery in November (25 thousand tons), to the month of April 2019 (5 thousand) and to the month of May 2019 (10.5 thousand tons). Much of the negotiated in these months is made with prices to fix.

During the week, a smaller commercialized volume of soybean was registered compared to the previous week (taking into account one less trading day in the week). According to official data, 41 thousand tons were negotiated with immediate delivery in the week of Friday 8 to Thursday 14. In the week of Friday 15 to Thursday 21 the negotiated tonnage reached 26 thousand tons. With the same trend, the negotiated by delivery in July was also lower than last week (108 thousand tons, against 320 thousand tons). 30% of what was negotiated was made to fix price, 24% was negotiated at AR$ 7,700 / t mainly on Friday 15 and another similar percentage on the AR$ 7600 / t. Regarding the forward segment, an important tonnage negotiated on the month of October (96 thousand tons) is observed. On Friday 15, close to 35 thousand tons were closed at AR$ 8,200 / t for delivery until that month, while the rest of the week, they closed forwards for 52 thousand tons at AR$ 8,000 / t. A lower amount was negotiated for delivery in November (25 thousand tons), to the month of April 2019 (5 thousand) and to the month of May 2019 (10.5 thousand tons). Much of the negotiated in these months is made with prices to fix.

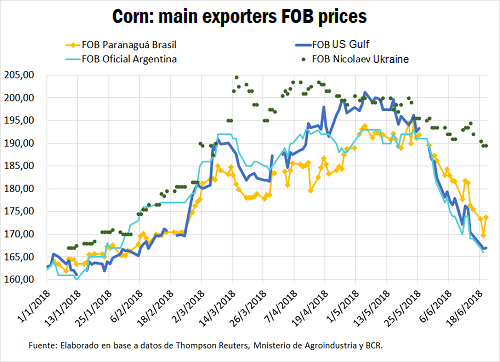

For its part, the price of local corn also fell sharply in the week. The Rosario Board of Trade´s reference price was equivalent to 156.20 USD / t on Thursday 21, noting a fall of more than 6 USD / t compared to Thursday 14. The fall in the price of corn in the last week is due to lower prices in the external markets. The strong attack that the oilseed received due to the US-China conflict, dragged the corn price globally, due to the pessimism generated and the spread maintained by both grains. With regard to marketing in Argentina, maize has a very high rhythm, as can be seen from the data released by the Ministry of Agroindustry on June 13. From the accumulated in the 2017/18 crop year it is observed that the export sector has acquired 12.84 Mt while the export commitments reach 12.96 Mt. That is, the export sector has more commitments of external sales than what they really acquired, what demonstrates a demand that remains robust for the Argentine cereal. It is precisely the external prices that limit the upward potential of the price of corn. The price of FOB corn fell $ 26 / t to $ 166 / t from the peak reached on May 23. Unlike soybeans, the commercialization of corn during the week did not suffer a drop (despite having a less commercial days). The negotiated volume of merchandise by immediate delivery reached 3,500 tons in the week of 15 to 21. It was, on the other hand, the volume of tons negotiated for delivery in July which maintained a very similar to last week. The total amounted to 202 thousand tons. The negotiated volume with prices to be fixed was small (5%), while a large part of the volume traded in Argentine pesos ranged between AR$ 4,300 and AR$ 4,500 / t for delivery until that month. The commercialization for the rest of the months and the new corn 2018/19 was almost nonexistent.

For its part, the price of local corn also fell sharply in the week. The Rosario Board of Trade´s reference price was equivalent to 156.20 USD / t on Thursday 21, noting a fall of more than 6 USD / t compared to Thursday 14. The fall in the price of corn in the last week is due to lower prices in the external markets. The strong attack that the oilseed received due to the US-China conflict, dragged the corn price globally, due to the pessimism generated and the spread maintained by both grains. With regard to marketing in Argentina, maize has a very high rhythm, as can be seen from the data released by the Ministry of Agroindustry on June 13. From the accumulated in the 2017/18 crop year it is observed that the export sector has acquired 12.84 Mt while the export commitments reach 12.96 Mt. That is, the export sector has more commitments of external sales than what they really acquired, what demonstrates a demand that remains robust for the Argentine cereal. It is precisely the external prices that limit the upward potential of the price of corn. The price of FOB corn fell $ 26 / t to $ 166 / t from the peak reached on May 23. Unlike soybeans, the commercialization of corn during the week did not suffer a drop (despite having a less commercial days). The negotiated volume of merchandise by immediate delivery reached 3,500 tons in the week of 15 to 21. It was, on the other hand, the volume of tons negotiated for delivery in July which maintained a very similar to last week. The total amounted to 202 thousand tons. The negotiated volume with prices to be fixed was small (5%), while a large part of the volume traded in Argentine pesos ranged between AR$ 4,300 and AR$ 4,500 / t for delivery until that month. The commercialization for the rest of the months and the new corn 2018/19 was almost nonexistent.