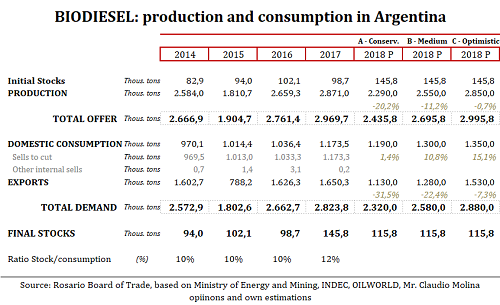

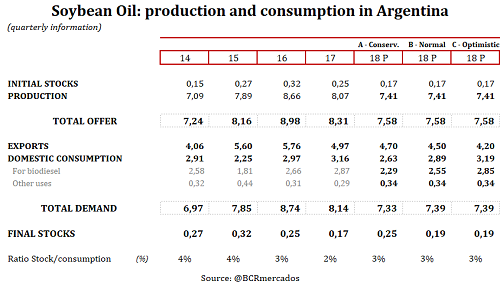

The biodiesel market is affected by a high level of uncertainty in the commercial policies applied by different countries internationally and the different government measures that could be adopted in Argentina. For this reason, regarding the year 2018, we proceeded to develop three scenarios, from one conservative to another medium and finally an optimistic one; according to the impacts of different measures that may affect the level of production and exports of local biodiesel. The main items to be projected were internal consumption, exports and production. Internal Consumption Conservative scenario: It coincides with the vision of both the United States Department of Agriculture (USDA) in its GAIN report of July 2017 and that of the Oil World Magazine of March 2018. The internal consumption of biodiesel in Argentina for the year 2018 was estimated at 1.19 million tons (this is approximately 1,350 million liters of biodiesel based on soybeans that will be incorporated into diesel as a mandatory cut). This would represent an increase of 1.4% over last year. Medium Scenario: Taking other variables into consideration, we project an internal consumption of 1.3 million tons (Mt). This scenario could be due to an increase in diesel consumption as a result of a higher level of economic activity (remember that the cutting of biodiesel for local fuel for automobiles is above 10% -B10). Bear in mind that the level of consumption of biodiesel by the electricity sector at present is 0%. Consumption could grow -in addition- because of the tax relief that falls on biofuel based on soybean oil through the new law of 27,430 in relation to "taxes on liquid fuels and carbon dioxide". Optimistic scenario: A much more optimistic projection would bring the consumption closer to 1.4 Mt, if the use in the automotive transport of passengers is increased, as a result of the implementation of the obligatory use of B20 for that segment in some important cities of the country. It could also increase consumption due to a rise in voluntary use in captive fleets. A decision by the National Government to increase the cut to B12 (12%) could help achieve this "optimistic" scenario, which is very necessary in the local biodiesel industry. The "medium" and "optimistic" scenarios at the consumption level become more difficult that can be concreted due to the fall in the production of soybean and corn (approximately 26 Mt) caused by the drought, which goes to generate fewer trips in trucking and rail transport of grains and less use of agricultural producers and Gas Oil contractors in the harvest. Exports The level of Argentine biodiesel exports will be determined essentially by what happens with the commercial policies of those countries that encourage the external market; mainly Europe, the United States and the rest of the world. Conservative scenario: Assuming foreign sales similar to last year to Peru plus exports that may come from Canada and a similar level to that exported to the European Union in 2014 (almost 1.1 Mt), we can estimate an external demand for the Argentine biofuel in 1,13 Mt. Medium scenario: It is estimated at 1,280 Mt. A medium term between the conservative and the optimistic scenarios. Optimistic scenario: According to the consultancy Strategie Grains, imports of Argentine biodiesel could reach 1.5 Mt in 2018. This scenario of volume of shipments is possible as long as the European Union does not apply measures against the Argentine Biodiesel. If total exports remain in 2018 by 1.53 Mt, it would still be 7% below the figure exported in 2017 and 2016. Production The Argentine production of biodiesel in the first two months of the year showed a good performance: record in historical terms with a little more than 400,000 tons in the two months. Maintaining the mandatory cut and the constant internal consumption estimates, it is observed that the greater or lesser production will come from the greater or lesser external demand for Argentine biodiesel. What happens in terms of consumption and exports will define the level of final production in 2018. Hence the estimated figures: Conservative scenario : estimated for this year at 2.29 Mt Medium scenario : estimated for this year at 2.55 Mt Optimistic scenario : estimated for this year at 2.85 Mt Soybean oil with lower prospects Soybean oil is the main input of the biodiesel industry in Argentina. Despite the fact that a greater demand for vegetable oils is expected by India, since the end of 2017 this country has been imposing high tariffs on imports, in a search to promote the local industrialization of oilseeds and their subsequent transformation into biodiesel. Argentina, among other countries, suffered this trade policy measure, decreasing shipments of oil to India. The lower export forecasts for soybean oil in Argentina will be made effective not only by a lower soy crop due to the drought, but also by a possible lower demand from abroad. Recall that India is the main buyer of Argentine soybean oil. While India's import tariffs on soybean oil have not changed in the recent update of March, it is important to note that the effective tariff has increased from almost 13% to 33% in recent years. While the intention to apply these tariffs is - ostensibly - to support domestic prices for oilseeds and the "Make in India" movement, it has logically attenuated the prospects for Indian vegetable oil imports in the current marketing year. Consequently, we estimate that the exports of soybean oil in our country in the current year will be located in a range of 4.20 to 4.70 Mt, according to the scenario. The production of soybean oil in Argentina can range between 7.4 and 7.5 Mt. We attach the soybean oil balance sheet, according to the Rosario Board of Trade´s estimates.

Rosario Board of Trade appreciates the participation in this work of the Executive Director of the Argentine Association of Biofuels and Hydrogen, Mr. Claudio Molina.