The agroindustrial chain tries to accommodate in a campaign devastated by the drought

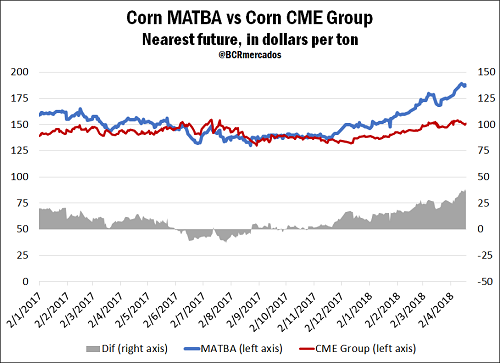

Corn prices in Argentina continued to be valued in relation to the US during the week, according to the references of the nearest futures in MATBA and CME Group, respectively. Thus, while the future in the Buenos Aires Futures Market adjusted on Thursday at US $ 188 / t, remaining the same as the previous week, the CME contract fell in the week US $ 2.66 / t adjusting on Thursday to US $ 150.39 / t.

This difference of US $ 38.39 / t last Thursday in favor of corn delivered to the ports of Rosario is much bigger than it was on January 1, 2018, of just US $ 7 / ton, so the gap quintupled in less than four months.

Regarding the first point, the Ministry of Agroindustry has published on Thursday its first estimate of Argentine production for the 2017/18 season, placing it at 42 million tons based on an area sown of 8.8 million hectares and a harvestable area of 6.7 Mha, while the average yield is calculated at 61 quintals per hectare. This volume of production is located 18% below the initial official forecasts. The Strategic Guide for Agriculture (GEA by its name in Spanish) service of the Rosario Board of Trade, meanwhile, kept its estimate at 32 million tons in the month of April, despite noting that with the results of the second threshing around the month of July there may be new changes in the final numbers, since they were the most affected varieties by the lack of water. It is worth mentioning that the Argentine Ministry of Agroindustry measures the total corn production including self-consumption in the farm, while GEA estimates the volume of commercial corn.

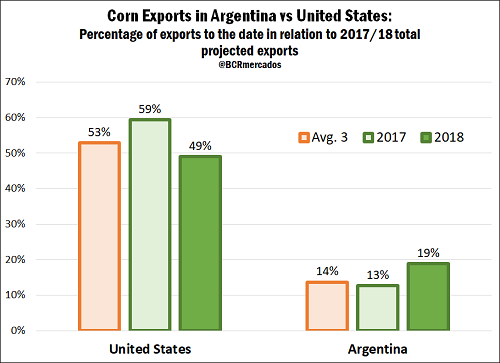

With respect to sales abroad, based on the load of ships reported by maritime agency NABSA, records to date show that the total volume dispatched and scheduled for the next weeks so far in the 2017/18 campaign amount to 6 million tons, above both the 4.8 Mt from last year and the 4Mt average recorded at this point of the last three years. In the United States, meanwhile, cumulative exports to date amount to 27.7 million tons, below the accumulated at the same date of the previous year (34.6 Mt), although in line with the average of the last three seasons (27.5 million tons).

If we compare those dispatch volumes with the total exports expected for the campaign in each country, Argentina exported or is close to exporting 19% of its estimated external sales for the entire year, when last year it was reaching only 13% of the exports planned for the whole cycle and the average of the last three years is 14%. Conversely, the United States has today exported 49% of what is projected to embark on the entire cycle, while last year it had already shipped 59% and the average of the last three years is 53%. As a note, it is worth clarifying that the 2017/18 corn campaign in the United States begins on September 1, while for Argentina it starts on March 1.

Over the last months, corn is being actively negotiated in the Rosario's physical market. There is a notorious interest of a large number of exporters to originate merchandise, while the range of offers arrives until the next 2018/19 campaign by values around US $ 165 / t for delivery in February / March 2019 and US $ 160 / t for June / July.

Regarding soybeans, this week the symbolic beginning of the commercialization of the 2017/18 campaign within the Rosario Board of Trade took place with the auction of the first batch arrived a few months ago. It comes from Formosa, and was acquired by the firm Puerto Arroyo Seco for a value of AR $ 15,500 per ton.

For the regular marketing of the oilseed, the prices stayed between stable and down in relation to the previous week. As of Thursday, the reference price of Rosario was AR $ 5960 / t, with a weekly loss of AR $ 270 / t. This fall is mainly due to the need of producers to deliver merchandise in a time when threshing machines are rapidly advancing, noting also that securing place for immediate discharge was a plus highly valued by the producers.

The strong advance of the harvest in our country, in the midst of the predominantly dry climatic conditions and the premature maturity of the grain, is reflected in the harvest advance data of the Ministry of Agroindustry. As a result, as of April 12, threshers would have advanced over 21% of the implanted area, versus the 9% advance registered at the same point last year. It is also highlighted that the Good and Very Good conditions reaches 58% and 33% of the crop, respectively, versus 61% and 41% in February.

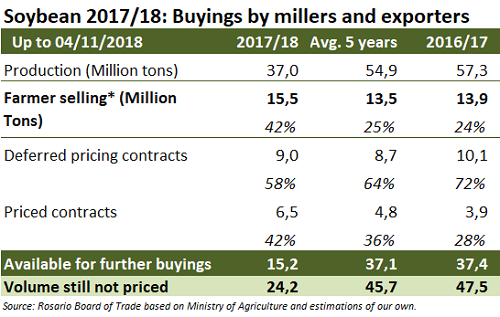

Under these conditions, the Ministry has reported its first official estimate of production, projecting a total soybean production of 37.6 million tonnes, based on a planted area of 16.7 Mha and a harvested one of 15.8 Mha. The average national yield, on the other hand, is estimated at 23.6 quintals per hectare. With these numbers, the output of the main crop in Argentina will remain 32% below the previous season as a result of the "worst drought in 50 years."

In this context, the interest of the soybean meal and oil factories to ensure the supply of beans for the coming months continues to be evident. Considering that the crushing capacity of the industry amounts to 66 million tons and that the national production would barely be around 37 million, even if all the stock stored in previous cycles were processed, there would be idle capacity. In this way, import operations have been verified, especially from neighboring countries, in recent weeks.

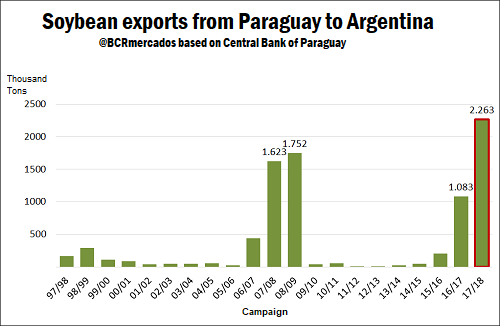

According to data from the Central Bank of Paraguay, during the month of March this country would have dispatched a total of 996 thousand tons, the highest monthly record in history, exceeding by approximately 550 thousand tons the second largest record that was the previous month (February 2018). Thus, in the first quarter of 2018 it is already imported 1.48 Mt more than what was imported throughout the year 2017 (1.4 Mt).

With the data of March, in addition, the total shipments of soybean of the campaign 2016/17 (that goes from April 2017 to March 2018) can be closed and would ascend to 2.26 million tons, a historical record in the bilateral exchange of this product. This value more than doubles the record for the previous campaign (1.08 Mt) and exceeds by more than 500 thousand tons the previous record that was established in the 2008/09 campaign.