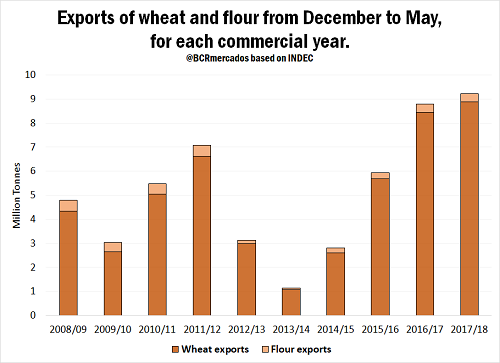

2017/18 wheat crop year is characterized by its accelerated pace of purchases, both from the export sector as well as from the milling industries. According to data from the Argentine Ministry of Agroindustry, as of June 27, 14.6 million tons of the cereal had been purchased, of which 11.2 were acquired by the export sector and 3.4 by the industries. Even with a production that was 700 thousand tons lower than the previous season, current purchases are surpassing those of last year at the same height. In this way, taking into account a production of 17.5 Mt, 84% of it has already been commercialized, that is, six percentage points above the previous year, and seven points above the average of the last 5 years. Therefore, at the aforementioned date, there are only 2.1 million tons of 17/18 wheat remaining to be negotiated, compared to 3.2 million tons last year. This could generate difficulties for certain supplies, both for consumption (human and industrial) as well as for export. The export profile of Argentine wheat is reinforced The sum of exports of wheat and wheat flour is widely higher than the average of the last years. Based on data from the INDEC (National institute of statistics), it can be observed that between December 2017 and May 2018, Argentina has exported 8.9 million tons of wheat and 343 thousand tons of flour, totaling 9.23 MT. This is 4.8% higher than what was recorded last year at the same height, and more than double the average of the last 5 years, which is 4.36 MT if cereal and flour are added.

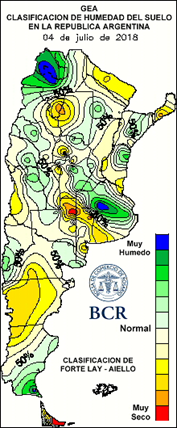

This context makes the supply of wheat 17/18 very tight in relation to demand, to the point that it is estimated that the final stocks could be among the lowest on record. As already mentioned, it will be difficult to solve the wheat origination problem to meet the needs of the demand. At least this will be the scenario until the 2018/2019 wheat begins to be harvested. With regard to prices Despite the advanced marketing of wheat so far this season, in the current week the local wheat market took a breather, being very quiet in our operations area. For spot wheat, there is only one buyer who can guarantee immediate delivery, while there are only a few who are demanding for delivery within the following 30 days. This lethargy caused the Rosario Board of Trade´s reference price to have a weekly decrease of ARS 50 / t, trading yesterday at ARS 5,900 / t. Contrarily, the futures for the new harvest of January 2019 were influenced by improvements in Chicago and had an upward week in the MATba (Buenos Aires Futures Market) for delivery in Rosario, with increases of 2.9% over the previous Thursday, closing on Thursday 5 in USD 186 / t. In the international reference market of Chicago, the nearest wheat futures were positioned in the bullish lane during the last week, achieving at the close of 5 th July, improvements of 5% compared to the previous Thursday. The main driver is the concern about the hardening of the global supplies of the grain given the adverse weather of the crops in reports from Western Europe and Russia, topics that will be developed later in this report. Good conditions in national fields The first lots planted with wheat are entering the tillering stage while much of the area passes through the emergence and foliation stage. The cold and dry environment discourages the proliferation of diseases without fungal difficulties and, in turn, benefits the work of harvesting soybeans to free lots for the sowing of winter cereals. As for water reserves, they are regular or scarce to the northeast of the country, on the contrary, in the center of the province of Buenos Aires they are abundant but without hindering the progress of the fieldwork. With an advance of sowing close to 80% to date, which exceeds the average of the last five years, it is very likely that the plans of 6.1 million hectares of wheat can be achieved.

This context makes the supply of wheat 17/18 very tight in relation to demand, to the point that it is estimated that the final stocks could be among the lowest on record. As already mentioned, it will be difficult to solve the wheat origination problem to meet the needs of the demand. At least this will be the scenario until the 2018/2019 wheat begins to be harvested. With regard to prices Despite the advanced marketing of wheat so far this season, in the current week the local wheat market took a breather, being very quiet in our operations area. For spot wheat, there is only one buyer who can guarantee immediate delivery, while there are only a few who are demanding for delivery within the following 30 days. This lethargy caused the Rosario Board of Trade´s reference price to have a weekly decrease of ARS 50 / t, trading yesterday at ARS 5,900 / t. Contrarily, the futures for the new harvest of January 2019 were influenced by improvements in Chicago and had an upward week in the MATba (Buenos Aires Futures Market) for delivery in Rosario, with increases of 2.9% over the previous Thursday, closing on Thursday 5 in USD 186 / t. In the international reference market of Chicago, the nearest wheat futures were positioned in the bullish lane during the last week, achieving at the close of 5 th July, improvements of 5% compared to the previous Thursday. The main driver is the concern about the hardening of the global supplies of the grain given the adverse weather of the crops in reports from Western Europe and Russia, topics that will be developed later in this report. Good conditions in national fields The first lots planted with wheat are entering the tillering stage while much of the area passes through the emergence and foliation stage. The cold and dry environment discourages the proliferation of diseases without fungal difficulties and, in turn, benefits the work of harvesting soybeans to free lots for the sowing of winter cereals. As for water reserves, they are regular or scarce to the northeast of the country, on the contrary, in the center of the province of Buenos Aires they are abundant but without hindering the progress of the fieldwork. With an advance of sowing close to 80% to date, which exceeds the average of the last five years, it is very likely that the plans of 6.1 million hectares of wheat can be achieved.

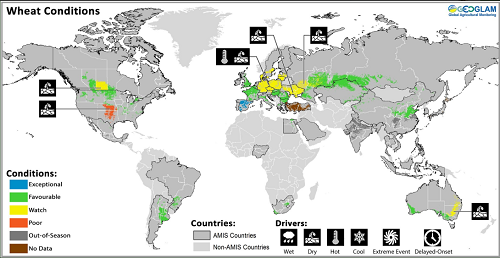

Disparity of wheat conditions between hemispheres In Canada (4th world exporter of wheat), recent precipitations along with normal temperatures gave relief to the areas of the west and south center that needed water. This scenario raises the projections of 2018/19 wheat production by 2% compared to the previous year, reaching 32.6 million tons. In the United States , above-average rainfall in the Plains in June improved the condition of the crop by propping up production estimates at 48.9 million tons, a rise of 1.6% over the previous year.

Disparity of wheat conditions between hemispheres In Canada (4th world exporter of wheat), recent precipitations along with normal temperatures gave relief to the areas of the west and south center that needed water. This scenario raises the projections of 2018/19 wheat production by 2% compared to the previous year, reaching 32.6 million tons. In the United States , above-average rainfall in the Plains in June improved the condition of the crop by propping up production estimates at 48.9 million tons, a rise of 1.6% over the previous year.

In contrast, in Russia , the spring wheat planting area falls and wheat production expectations for 2018/19 are reduced by 1% to 71.3 million tonnes. However, the country has high stocks from previous harvests. The same unfavorable scenario occurs in the European Union , where the continuous dry weather in the northeast of the region reduces the expectations of 2018/19 wheat production. The European Union could harvest almost 6 million tonnes less of wheat this year after crops in the northern part of the bloc suffered a warm and dry spring, as well as late signs of crop damage in the main producer of the Union, France, according to a Reuters poll. With regard to the latter country, the consulting firm Strategie Grains reduced its estimate for the French wheat crop by 4.6 million tons to 33.2 million, since the heavy rains of winter and last month damaged the development of the plants.

In contrast, in Russia , the spring wheat planting area falls and wheat production expectations for 2018/19 are reduced by 1% to 71.3 million tonnes. However, the country has high stocks from previous harvests. The same unfavorable scenario occurs in the European Union , where the continuous dry weather in the northeast of the region reduces the expectations of 2018/19 wheat production. The European Union could harvest almost 6 million tonnes less of wheat this year after crops in the northern part of the bloc suffered a warm and dry spring, as well as late signs of crop damage in the main producer of the Union, France, according to a Reuters poll. With regard to the latter country, the consulting firm Strategie Grains reduced its estimate for the French wheat crop by 4.6 million tons to 33.2 million, since the heavy rains of winter and last month damaged the development of the plants.